LIFTING-THE-BARRIERS REPORT 2013 | FINANCIAL SERVICES

Published date: November 2013

TABLE OF CONTENT

(Click any topic to read the related section)

- 1.1 Executive Summary

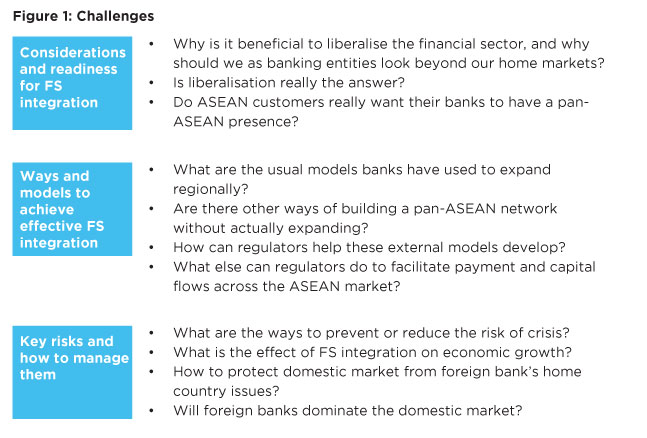

- 1.2 Key Challenges for ASEAN FS integration

- 1.3 Lifting-The-Barriers – Exploring solution to the actual and perceived barriers

- 1.3.1 The PAN ASEAN Banking Pass

1.3.1.1 Overview

1.3.1.2 Benefits of ASEAN Pass

1.3.1.3 The way forward - 1.3.2 Free Talent Mobility

1.3.2.1 Overview

1.3.2.2 Benefits of Talent Mobility

1.3.2.3 The way forward - 1.3.3 ASEAN Alliance model

1.3.3.1 Overview

1.3.3.2 Benefits of Alliance models

1.3.3.3 The way forward - 1.3.4 Building Common Credit Bureau Infrastructure

1.3.4.1 Overview

1.3.4.2 Benefits of having a common credit bureau infrastructure

1.3.4.3 The way forward - 1.3.5 Common Credit Rating Agency

1.3.5.1 Overview

1.3.5.2 Benefits of having a common credit rating agency

1.3.5.3 The way forward - 1.3.6 Free Data Flow/Off-shoring

1.3.6.1 Overview

1.3.6.2 The key benefits of off-shoring and free data flow

1.3.6.3 The way forward - 1.3.1 The PAN ASEAN Banking Pass

- 1.3.7 Standardisation of Nomenclature, Documentation, and Common Infrastructure

1.3.7.1 Overview

1.3.7.2 Benefits of standardisation

1.3.7.3 The way forward

1.1 Executive Summary

Financial services (FS) throughout South-East Asia remain extensively regulated, some of which are restrictive to regionalisation. To address that, a key component of the ASEAN Economic Community (AEC) 2015 vision is the liberalisation of financial services. Different parties bring different views on the pace and benefits of financial integration. Industry and trade organisations, for example, believe financial integration can accelerate economic gains, lower regionalisation costs, and help small and midsize enterprises (SMEs) become more competitive. Regulators and local governments worry, however, that integration may expose the region to unwanted volatility and that the economic benefits may not materialise as swiftly as promised.

Among the key questions for stakeholders are:

In weighing those questions, several factors come into play. Banks, governments, and regulators will need to have an open discussion on a number of important challenges. Chief among them are:

- Heterogeneity of regulatory frameworks and restrictive market access within ASEAN;

- Constraints on talent mobility;

- Regulatory limitations on cross border data flow and off-shoring;

- Impediments to Pan Asia trade flow and focus on China and India;

- Lack of standard infrastructure to facilitate cross border credit;

- Lack of standardisation across region with respect to operational process and common infrastructure

The regional growth in ASEAN trade coupled with Asian growth and concentration of trade corridors and global uncertainties have made banks to be competitive. Indeed, many strong banks will choose to remain and grow domestically as fits their strategy, however for banks with regional aspiration it is important to grow and expand regionally by being scalable and big. Such growth and expansion requires a common yardstick and basis that will drive the growth, expansion and liberalisation of the sector. Hence the key question is identifying the common yardstick to discuss the right set of liberalisation measures.

It emerges from several discussions with industry leaders that customer value is the yardstick by which regulatory and other liberalisation changes must be measured. As banks and regulators gauge their course, the driver must be the extent to which cross-border access and regulatory integration will benefit customers in the region.

Standard Chartered bank provides one example of a customer-led approach. Their growth strategy segmented geographies into (i.) core markets (Hong Kong, Singapore, Korea, UAE, etc.); (ii.) city-focused markets (including China, India, Thailand, etc.); and (iii.) niche markets (smaller countries ranging from Bahrain to Brunei). That segmentation allowed them to tailor services and products to specific market needs, such as introducing “15-minute loan approvals” in Hong Kong, innovations that allowed them to compete successfully in a number of different areas across the region.

A similar, customer-centric rubric is needed to advance liberalisation within financial services.

End-customer benefit and performance measures

Integration will deliver three primary customer benefits, each of which can be measured.

- Better Service: providing greater choice to the customer, by expanding access to a wider array of products and services, and cross-leveraging other offerings, such as wealth management services

- Better access to credit: providing corporates and SMEs with greater access to credit for domestic expansion and cross-border trade

- Cheaper banking services: channelling cost and operational efficiencies into improved service and value for customers

Ideas to break the barriers.

Recent interactions with senior banking executives in the region generated these seven ideas.

- Pan-ASEAN Banking Pass

- Free Talent Mobility

- ASEAN Alliance

- ASEAN Credit Bureau

- ASEAN Rating Agency

- Free Data flow/Off-shoring

- Standardisation of documents/ Documentation requirements

Addressing these ideas should confer real benefits to the end customer and economic benefits to the region at large. They provide a basis for regulators and banks to discuss how best to bring about the changes needed.

1.2 Key challenges for ASEAN FS integration

Ideas to break the barriers

The current regulatory environment means new entrants face steep, sometimes prohibitive investment requirements, forcing some to invest at an extremely high level and others to make sub-scale investments, neither of which is profitable for the bank, good for customer or sufficient to spur economic growth.

To be cost and market competitive, banks must be able to leverage their infrastructure and talent base. Regulatory restrictions around talent mobility, the free flow of information, and offshore activities hinder the type of scale efficiencies and process standardisation that can improve cost and risk performance and customer service. In addition, banks must have the ability to extend credit to facilitate the expansion of the real economy. But, the lack of “comparable” credit and rating bureaus across ASEAN curbs lending.

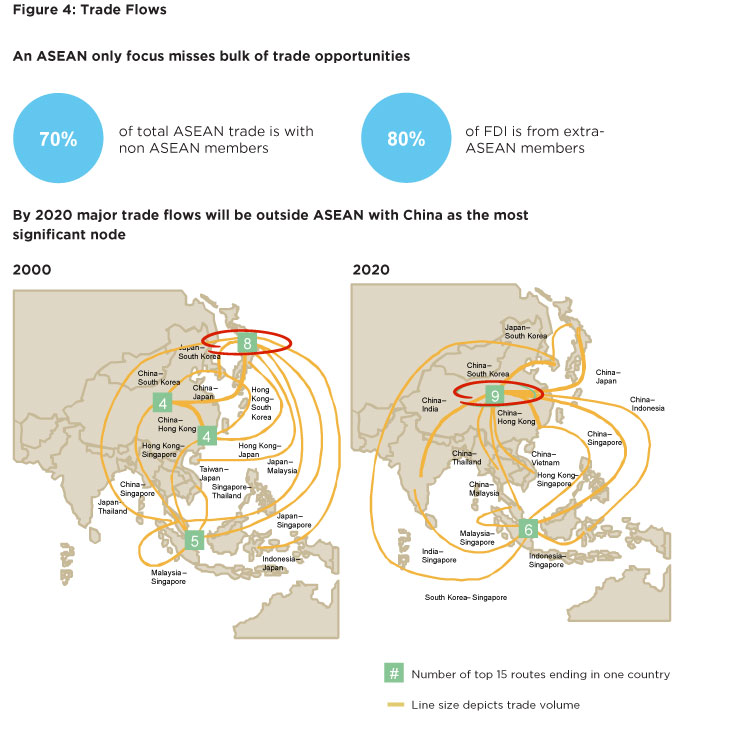

As trade corridors widen between China, India and ASEAN, banks forced to operate at sub-scale handicap ASEAN companies that rely on strong and scalable banking services to expand into adjacent markets.

A breakdown of the key challenges follows.

- Heterogeneity of regulatory framework and restrictive market access

Inconsistent regulatory regulations have hindered the expansion of banks within ASEAN. For instance, Bank Mandiri’s potential entry and expansion into Malaysia, was stalled by the amount of paid-up capital required (US$96M, -10X Indonesian standards), a figure deemed too high by Mandiri. DBS abandoned its planned acquisition of Danamon given the conditions for reciprocity and newly-imposed limits to foreign ownership (maximum of 40 percent) imposed by Indonesia. Maybank, another regionally active player, also had challenges with its acquisition in Indonesia, due to regulatory changes on free-float requirements (minimum of 20 percent), post deal completion.

The Indonesian central bank issued regulations that require banks to open one branch in a tier 5-6 location for every three branches they open in a tier 1 city, notwithstanding the strict capital requirements that make adding more branches potentially uneconomical. The central bank also intends to require foreign banks to be locally incorporated and may impose restrictions that limit direct foreign investment in domestic banks to a maximum 40 percent. Such changes will likely reduce foreign bank interest in Indonesia.

Rules in the Philippines cap the number of foreign banks permitted at any one time to 14. Thailand used to ask foreign banks to hold at least 10 billion Thai baht as Tier 1 Capital, compared to five billion THB for local banks in addition to restrictions on the number of branches a bank could opened annually.

In most cases, national regulatory frameworks limit ASEAN financial institutions — as well as foreign financial institutions — from expanding quickly.

2. Constraints on talent mobility

The flow of talent is critical for regional economic development. Within Asia for example, Singapore has leveraged talent mobility to its advantage. It is a relatively easy place to relocate to. Residency rules are becoming more lenient. In some cases, it can take as little as one day to get a working visa, depending upon the assignee’s nationality, salary level, and qualifications. Those developments have allowed Singapore to attract and retain highly qualified talent. But, Singapore remains a fairly isolated example.

Across most of ASEAN, talent mobility remains a key concern. Region-wide barriers, such as the lack of a common framework for skill recognition, differences in the quality of educational institutions, visa restrictions to protect domestic employment, and licensing (e.g. national professional-association licenses) are among the major impediments.

3. Cross border data flow and off shoring regulatory constraints

Harmonising the regulation of cross border data flows, technology operating models, off-shoring and data centre sharing, is key to process integration and regionalisation. Currently, regulatory differences concerning customer data make it hard for banks to share basic information. For example, Bank Indonesia is pushing banks to locate core banking systems in-country. But, many foreign banks will find limited cost efficiency in this model. There is an inherent difference in the way local and non local banks process, handle and distribute personal data and a one-size-fits-all approach that prohibits global systems, restricts data sharing outside jurisdictions for all scenarios and prevents banks from accessing important new technologies will disadvantage customers and slow growth.

4. Pan Asia trade flow and focus on China and India

Trade corridors are changing, with China, Singapore and India emerging as hubs. The subscale operations in the region coupled with strong domestic players in the major markets will make it difficult for ASEAN banks to grow as Pan Asian banks. Organic growth is a bigger challenge since these markets are highly competitive with numerous players e.g. the largest ASEAN bank is smaller than the 50th Chinese bank in terms of asset size.

5. Lack of standard infrastructure to facilitate cross border credit

ASEAN’ s heterogeneous liquidity needs make it vital to have a strong credit information and ratings system, one that standardises key processes and practices to improve quality, accuracy and decision-making on the credit side.

6. Lack of standardisation across region with respect to operational process and common infrastructure

Currently there is no standard infrastructure or standards for common process such as Know Your Customer (KYC) infrastructure which increases bank operational costs and limits the ability of banks to transfer the benefits of integration over to the end customer.

1.3 Lifting the Barriers: Exploring Solutions to the Actual and Perceived Hurdles

We explored seven key ideas in conjunction with key banks in the industry to overcome these issues and drive greater customer returns.

1.3.1 The PAN ASEAN Banking Pass

1.3.1.1 Overview

A Pan-ASEAN banking pass would give customers the benefit of best practices across markets and better pricing and rates from a combination of scale efficiencies, better collaboration and information sharing, and greater operating breadth to help ASEAN companies expand into India and China.

However, regulators need assurance that free access into their markets would not jeopardise the growth of domestic players, or destabilise economic growth. They worry, for instance, that foreign banks could potentially skim the cream and leave local banks with riskier and more structurally unprofitable business without the ability to cross-subsidise. They’re concerned also that too much foreign influence might make it harder to steer the banking sector in the event of a crisis.

These are complex issues and no one answer will suit all markets. That said, there are enough regulatory measures already on the books to mitigate some of these concerns without restricting market access, such as directed lending towards specific sectors for all banks, full subsidiarisation, and trapped liquidity pools.

It’s important also not to underestimate the strengths of the local banks in withstanding increased competition. For one thing, domestic banks have outperformed their peers with regional aspirations. For another, the barriers of entry are already sizeable in terms of installed infrastructure and available risk capital even without any additional regulatory constraints. For aspirants, achieving regional scale will require they make additional investments before they can reap the benefits. In light of these challenges, leading local players express very limited concern about the prospect of regional competition.

As a result, regulators may find it more valuable to focus on creating a common pan-ASEAN framework under which “qualified” banks can freely operate across ASEAN, then leave it to the customer and market competition to determine how banks will use that freedom. It can be expected that the business case justification will mean only a handful of banks will apply for an ASEAN license to expand. Once there, competitive pressures will force all players to innovate and provide better value to customers, which is the ultimate regulatory objective.

By way of example, the Eurozone began regionalisation with many strong domestic banks. Over time, strong regional banks emerged to join that field.

Banks such as BNPP, Unicredit, and Santander went across borders to tap the trade corridors. They expanded branches and subsidiary networks regionally. Some of these banks are now growing globally, using their experience and capabilities to scale up.

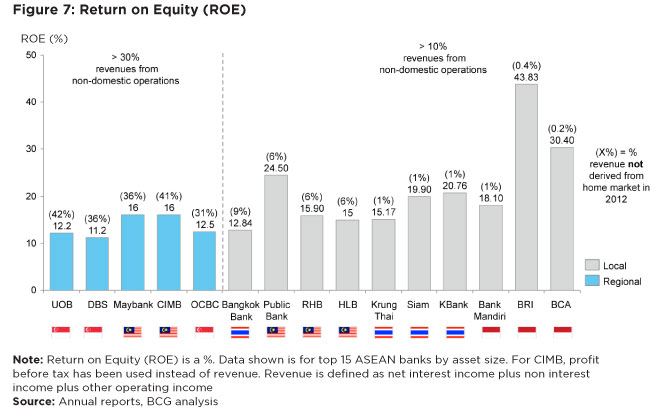

Within ASEAN, several banking and FS institutions with strong domestic focus have posted strong financial performance (return on equity – ROE) and shown potential for continued growth. They could be in a strong position to follow the example of their European peers.

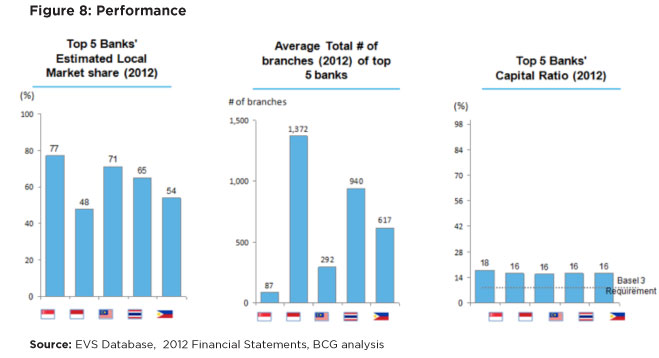

Additionally, the top banks in each of the original five ASEAN members command a dominant share of the market, and are better capitalised than Basel III norms mandate. As one can see, to match the network of the incumbents in these markets where branches are still important to building a sustainable franchise a newcomer will have to make substantial investments to pose any significant threat.

Singapore’s aviation sector offers a good example of the effect that a liberalised financial sector can have. Singapore is one of the few countries in the world that have instituted an “Open Skies” policy. This means that any airline from any country in the world has the right to fly in and out of Singapore. This has led to the emergence of Singapore as a global hub of international passenger traffic. Those free-entry policies had a positive impact not only on the domestic market, but on domestic players as well. The national carrier, Singapore Airlines, has performed well in comparison to regional competitors in terms of net profits.

This example demonstrates that openness with the right policy can help banks with strong domestic footholds compete effectively with new entrants and potentially become regional players.

Regional players can emerge by scaling up through freer access

Banks with regional aspirations can achieve better CI and higher ROE by being allowed to scale up and expand quickly. Some banks that have already embarked on regionalisation have built the right capabilities, fostered innovation, and enjoyed strong domestic presence.

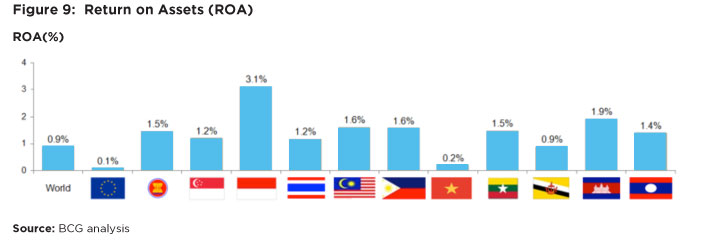

As a region, ASEAN banks have achieved strong performance. ASEAN’s Return on Assets (ROA) is an impressive 1.5 percent, higher than the world and EU averages of 0.9 percent and 0.1 percent respectively. Gross non-performing loans make up 2.11 percent of ASEAN bank balance sheets, beating the world and EU figures. Furthermore, Capital Adequacy Ratios in ASEAN, at 20 percent, are on average 5 percent higher than in the world and EU.

ASEAN banks have well-financed balance sheets with more-than-adequate capitalisation and reserves. Such financial health puts players in a strong position both to compete across ASEAN and withstand the entry of additional competitors within their domestic markets.

Some players, such as DBS, OCBC, CIMB, MayBank, Bangkok Bank, and Standard Chartered are already trying to build a business model for regional economic integration by pushing their presence in every market in ASEAN.

The potential of banks to grow regionally and the need to go regional in light of changing trade corridors are critical factors in encouraging banks to scale up. Regulators should create a common pan-ASEAN framework under which “qualified” banks can freely operate.

1.3.1.2 Benefits of ASEAN Pass

The key customer benefits from an ASEAN bank pass include:

A wider product range: Banks with strong domestic businesses, such as those in Malaysia and Singapore, can introduce their sophisticated high-end products into other ASEAN markets.

More choices per product: Regional banks can provide more trade, cash-management, financing products, and payment products (e.g. ASEAN wide procurement cards). They are also better placed to manage supply-chain and liquidity requirements.

Better access to credit internationally: Established customers can gain easier access to cross-border credit. In returns, central banks could mandate that all banks dedicate certain portions of their loan books to politically sensitive sectors.

Lower fees: Free access to other regional markets allows banks to achieve regional economies of scale (operational cost). The channel experience can be optimised. Hence, “R&D” costs for innovative models across several markets will help lower costs for end customers.

1.3.1.3 The way forward

The idea of an ASEAN passport is not new. In fact it forms part of the ASEAN banking integration framework. However, progress in making the Pass program a reality so far has been limited and may not be sufficiently comprehensive.

The ASEAN Banking Integration Framework was intended to address such issues. Authorities from the 10 ASEAN central banks agreed upon four preconditions to ensure that a framework was successfully implemented. One of these preconditions was establishing set criteria under which ASEAN qualified banks could operate in any ASEAN country with a single “passport.” Under the ASEAN Banking Integration Framework, each ASEAN member country will be able to designate one or more local banks as a Qualified ASEAN Bank (QAB) that is able to expand and operate within the region. The number of banks so designated will depend upon the agreement between ASEAN countries.

While these moves are a step in the right direction, they do not go far enough. For instance, the QAB framework does not address the standing of multinational banks that have been in the region longer than many domestics and have played a critical role in enhancing the financial system in core ASEAN markets. Moreover it requires alignment and consensus across all markets and it will be difficult to achieve consensus among members and comprehensive criteria may be difficult to achieve in one go.

More thinking is needed to drive better alignment and consensus across all markets. Given the complexity, a phased approach can be adopted whereby banks are evaluated through a comprehensive set of criteria to gauge a bank’s overall strength and readiness. Such criteria could include:

- Financial performance: Key financial ratios on capital, profitability (cost-to- income), liquidity, and shareholder value

- Customer centricity: Satisfaction, complaint management, and security

- Operational strength: Ability to scale up and increase connectivity

- Innovation: Platform, products, improving financial inclusion etc.

- Regulatory and compliance track record: Non-submission, non-compliance to local regulation, lapse in AML, and local compliance systems etc.

- History: Length of stay in a country and commitment to economic contribution

- Ownership structure: Shareholding pattern

- Onshore talent

This model should be utilised to promote a fast-track process for banks to obtain an ASEAN pass without subjecting qualified banks to stringent regulatory restrictions.

The final criteria should allow at least one bank from each ASEAN country to qualify for an ASEAN pass, rather than adopting a “wait until a comprehensive ASEAN pass emerges” approach. That’s because building banks that have regional stature and integrating financial infrastructure will precede regulatory harmony.

Alternatively, one form of phasing could allow some core countries, such as Singapore, Malaysia, Thailand, Indonesia and the Philippines, to grant a limited number of qualified banks with complete access to certain markets with no discrimination between local and foreign banks. That would mitigate “overpowering” the local banking system because it would force entrants to innovate to compete for customers and allow strong domestic banks to expand into other markets. Over time, as banks and financial systems strengthen, other banks and countries could join this framework.

1.3.2.1 Overview

Talent mobility is an important element of financial services liberalisation. Several key banks in the ASEAN region have faced significant difficulty in hiring non-citizens for key positions within their firms. Regulatory restrictions on talent mobility may at times hamper the realisation of the AEC vision, because it restricts banks from accessing the best human capital that is available in the region.

In a heterogeneous labour market, there are bound to be skills gaps. It is essential to make use of the superior skills that are available in the region in order to build capacity and expand. There will be a tremendous need to train local talent and build the required competencies. Efforts should therefore be made to allow mobility and to promote knowledge transfer. The free movement of talent can bring the following benefits:

1.3.2.2 Benefits of Talent Mobility

By accessing a regional/global talent pool (either by hiring and/or transfer of people with respective expertise) a bank can:

- Introduce a broader and deeper product set faster and more effectively. Customers gain better service, faster access, and well-developed products only when banks are able to scale up, improve their technology and innovation, and offer a variety of popular/tailored global products in the local market. To execute this, banks need to hire local, regional, and global talent and/or transfer talent with the required capabilities into new markets to help build up those businesses. When it comes to more-sophisticated models and products, talent is usually the limiting factor.

- Foster Innovation. Recent banking innovations have been coming from emerging-market countries. Transfer of business model innovations can help them reap economies of scale on investments made in intellectual property, systems, and capabilities.

- Result in Economic growth. Talent will be deployed where it can create most economic value. For example, there are several markets in the Euro region with high unemployment (e.g. Spain), while the demand for talent in others (e.g. Germany) is high. Talent mobility helps bridge the gap between the supply (Spain) and demand (Germany) to a point where growth is lifted.

The ASEAN region must develop a self-sustaining ecosystem that puts plans and programs in place to address skills gaps before they become critical. Given the complexity of regional language needs, differences in standards of education, and the long timeframes over which interventions occur, getting the right degree of coordination and long-term investment is crucial.

Overcoming these barriers and increasing mobility requires a number of initiatives among organisations and policy makers. Here’s how these changes could be phased in over time.

- Short-to-medium term

Fill the skills gap by forging a simple regional visa policy

To meet the current talent crunch in ASEAN FS, a special quota that is pre-approved for banks, and based on key criteria (such as minimum years of presence in a country) would be a useful stop-gap and should be accompanied with a fast-track process for key FS roles.

Streamlining and simplifying processes to secure work permits, removing national visa barriers, and even developing one regional work permit could help bridge skills gaps and grow competencies on a local level. The European Union, for instance, established a Blue Card scheme to attract highly-skilled migrants from outside the region. The Blue Card provides a two-year single work and residency permit across member states. Supporting actions include a streamlined and centralised visa application process and a travel permit to member countries for the holder and his or her family.

In addition, a pan-ASEAN travel card similar to the APEC Bus Travel Card should be open to all nationalities, especially senior executives of ASEAN companies.

2. Medium-to-long term

Encourage companies to promote mobility within their own organisations/subsidiaries. Allowing regional and multinational banks to hire local talent, offering on-the-job training, and placing people back in their home markets in ASEAN can help leverage their learning, improve competency, and build skills.

Moreover, allowing regional banks’ headquarter people to be placed in local markets, and creating a link with HQ for closer understanding of that market, can result in strong leadership. It can also enable top foreign talent to train senior management. Korean companies such as Hyundai, Samsung have followed these principles and been successful.

In addition to enabling better mobility, ASEAN countries should set up high-quality training institutes using senior bankers as instructors, define certification mechanism, and create guidelines to recognise qualification across border. These will create early involvement in the talent pipeline around specific skills (e.g. risk, finance, and payments).

Regulators should give banks incentives (e.g. tax breaks or grants) if they can show that they develop local talent for critical positions.

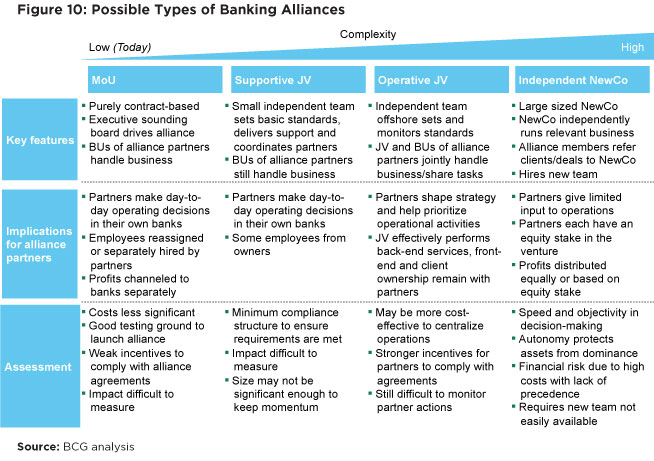

Regional strategies often focus on integrated regional banks. However, alliance models are also beneficial. In fact, the traditional network of correspondent banks has been a proven concept for cross-border banking for several years. More recently, we have seen established networks, such as KBank’s partnership with local banks in ASEAN under the Asian Alliance model. These alliances are simple and focused mainly on trade financing and simple referrals. Other industries have pursued more complex alliance models. The “Star Alliance” in the airlines industry, for example, is more far reaching, encompassing everything from using joint infrastructure and joint purchasing to joint IT platforms and development.

Banking could take a similar approach. While banks have adopted different alliance structures, grouped around product, geography, and sales, they could go farther, employing risk diversification by joint underwriting of large loans using cross-country club-deals, syndication, deploying excess liquidity and leveraging joint infrastructure such as processing centers or training centers for senior executives, creating joint capability hubs for areas like asset management or wealth, among other initiatives.

For such a model to work, however, regulations will need to flex accordingly ensuring steady cross-border lending flow and liquidity across the region.

1.3.3.2 Benefits of Alliance models

Value creation in the alliance model can come from many sources:

Better access to credit domestically.Many of the largest clients (mostly conglomerates) are hitting single-customer limits. It would be easier for a group of ASEAN banks to finance these large exposures through club deals. That would create better risk diversification while still reducing costs for customers (compared to the traditional cross-country syndicated loans arranged by multinational banks).

Better access to credit internationally. It is much easier to facilitate cross-border access to credit for established customers without resorting to regional and MNC banks only.

Lower cost to customers. Alliances can facilitate lower costs for operations since the need for fixed investment in subsidiary branches is negated. Shared technology platforms and investments can decrease the cost of sales and increase cross-selling percentage.

For alliances to succeed, banks need to carefully evaluate whether their business models are suitable to capitalise on the growth of intra-regional trade and willingness to commit to the alliance. This is because existing initiatives demonstrate the benefits of potential alliances to banks and regulators; that it benefits customers by engaging in cross-border business. For new alliances on liquidity, joint underwriting of large loans formalising these syndicate arrangements, allowing direct foreign currency loans can constitute the initial steps toward a more comprehensive alliance model. For most regional level alliances there will be sharing of resources, infrastructure and systems. To make this happen, regulators should allow building of such common IT platforms, regional infrastructure for processing training, facilitating cross border customer information sharing especially involving common data infrastructure (data centres, core systems). A liberal regulation on resource-sharing, setting up business-matching services, allowing talent mobility and customer referral can support the alliances and make them successful, allowing banks to focus on creating value to the customer.

1.3.4 Building Common Credit Bureau Infrastructure

1.3.4.1 Overview

Access to credit across the SME, corporate and consumer segments is a growing need. This is especially true for SMEs, which represent the largest non-agricultural business block. While the credit needs of large corporations tend to be well served by major domestic and global banks, the majority of SMEs in developing nations rely on informal financing, such as family, community and private financiers. Those informal channels are insufficient to support cross-border, intra-ASEAN trade growth. To expand credit access across all segments, a common credit bureau infrastructure must be built.

That infrastructure must reflect the needs of both credit applicants and lenders. On the demand side, for instance, SMEs and others require a more systematic disclosure of financial and performance information, governance and business planning, and promoter’s credibility. On the supply side, banks and regulators must rely more on credit information systems and find common ground on credit bureau governance, make SME risk scoring more pragmatic, and engage in benchmarking of similar SMEs sub segments.

However empirical evidence suggests that a strong credit bureau system can remove these obstacles. For example, A World Bank policy survey of 5,000 SME firms in 51 countries (Love & Mylenko, 2003) found that:

- SME reporting constraints were 22 percent lower in countries with credit bureaus, than those without

- SMEs were 12 percent more likely to receive loan approval in cases where there was credit bureau input

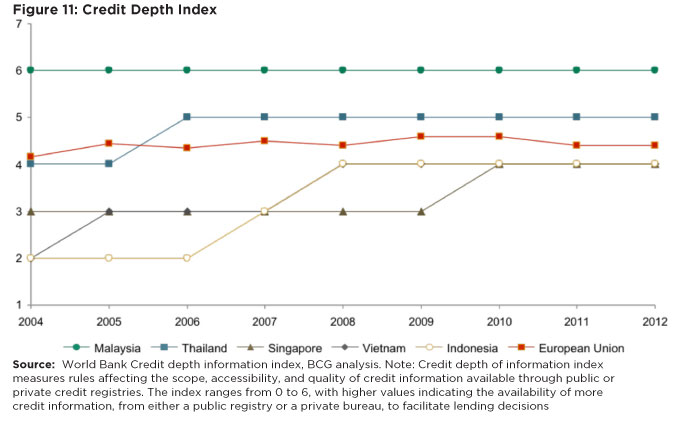

Bringing credit processes and standards to a common, high standard across the region is an important pre-condition for a strong credit bureau infrastructure. World Bank data shows that the depth of credit-related information currently varies widely. This exhibit suggests that Malaysia’s credit depth, which is the best in the region, could serve as a useful starting point to conform best practice standards.

Several private credit bureaus also operate in ASEAN in places like Malaysia, Philippines, Singapore, and Thailand, although relatively few offer public credit registers, Indonesia, Malaysia and Vietnam being among the exceptions. Such heterogeneity limits the quality and availability of information-sharing, particularly with respect to SME lending.

1.3.4.2 Benefits of having a common credit bureau infrastructure

Having a common or centrally-governed credit bureau system with access to similar information in all markets has several benefits:

Better access to credit domestically and internationally. Creating a common credit infrastructure would ease the lending process, allow banks to reduce operating costs, and reduce average lending rates. A universally understood framework for risk assessment would also allow more banks to provide credit to companies internationally. Such benefits have already been demonstrated in Eastern Europe, for example, where leverage ratios are 4.2 percent higher in countries where credit information sharing is more prevalent.

Lower risk cost. Better transparency would improve risk management practices, reduce NPLs/credit losses, and lower rates to customers. A centralised credit bureau would also act as an enforcing mechanism, pushing clients to pay or be listed as a bad risk. For example, in Shanghai, NPL ratios were reduced from 6.67 percent to 4.52 percent in the year after a local centralised credit bureau was launched.

Greater product penetration. Apart from reducing defaults, centralised credit bureaus can identify SMEs and other clients with good credit records. Banks can target these higher value companies with greater product choice and a wider array of credit offers.

Common credit bureaus bring other benefits as well, such as common standards in due diligence, the establishment of risk benchmarks (which are unavailable at the moment, especially for SMEs), and the prevention of fraud/money laundering through widespread and cross-border information sharing.

1.3.4.3 The way forward

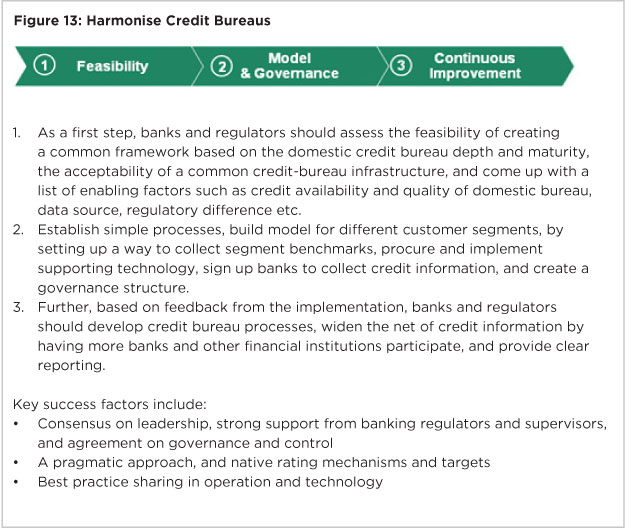

The following steps can help ASEAN establish a common credit bureau infrastructure that over time can function as the repository of all relevant credit information for corporates, individuals, SMEs, and microfinance borrowers.

i. Leverage best practices across markets to create a national infrastructure based upon uniform standards. Gaining insight into those best practices will involve collaboration within ASEAN nations.

ii. Harmonise credit bureau infrastructure and information across the ASEAN markets to facilitate cross-border activities. That type of body could be jointly run by regulators and banks and set up either as a separate entity or as part of an existing agency. In Europe, for instance, the ECB governs several credit institutions, but does not have a central credit bureau.

1.3.5 Common Credit Rating Agency

1.3.5.1 Overview

Ratings are key to opening up capital market intermediated funding for several reasons. One, there is growing need for capital markets intermediated funds. Two, the capital and bond markets are highly fragmented currently. And three, commercial banks are likely to continue to play a dominant role in financial intermediation. All that makes the need for credit rating capabilities in all ASEAN countries that much more important.

To date, global rating agencies have filled some of this void. But, the global financial crisis exposed some of their limitations, especially on structured products, factors that have helped make the case for a new, regionally-focused rating agency.

Setting up a regional rating agency will be very difficult. For one thing, a strong regional rating agency depends on a strong network of local or domestic credit agencies and ASEAN countries are at varying levels of development in this area. There are also larger, structural issues that need to be resolved. They include differences in domestic bond markets, accounting and disclosure standards, legal and regulatory frameworks, and sovereign risk. Such differences mean that in some cases establishing common benchmarks may not be feasible.

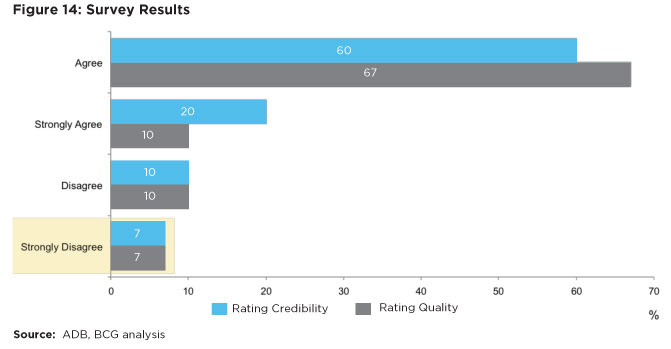

The idea of a regional rating agency structure, however, does have precedent. Europe proposed an initiative to establish a European Rating Agency a few years ago. The goal was to build a regional entity that would compete with US-based equivalents such as Standard & Poor’s, Moody’s and Fitch, be financially independent (unlike their U.S. peers), and feature more players and market competition. To promote transparency and independence, the proposed model would be led by a consortium of investors that included stock exchanges and credit institutions as well as private, non-profit foundations with a strong academic council. As an additional check, the model also called for a special oversight agency to ensure public monitoring. Although the idea failed to get off the ground due to questions over the right financing model and governance, it serves as an interesting framework for ASEAN to consider. In a survey conducted by the Asian Development Bank for Development of Regional Standards for Asian Credit Rating Agencies, (See Figure below), 80 percent of domestic credit rating agencies agreed that harmonisation would enhance their credibility and help improve rating quality.

The report also points out that:

- A region-wide ASEAN Bond Market would fuel demand for regional ratings and the need for cross-border comparability of domestic ratings

- Domestic Credit Rating Agencies (CRAs) could capitalise on these opportunities using their in-depth knowledge and familiarity with the local environment

- Domestic CRAs could better serve SMEs and smaller issuers with relatively lower rating fees

A common regional credit rating agency would facilitate the development of capital markets, provide banks with a view on the strengths of SME customers, and help channel regional savings to regional investment. The Association of Credit Rating Agencies in Asia (ACRAA) is one such initiative in which 25 CRAs from 14 countries/economies are members. They aim to develop and maintain cooperative efforts among credit rating agencies in Asia and could be instrumental in creating common standards.

1.3.5.2 Benefits of having a common credit rating agency

There are several benefits to having a common credit rating agency:

Better access to credit domestically. A regional agency essentially converges different rating-agency practices into a standard one. By leveraging the experiences of markets such as Thailand, Malaysia and Singapore in other ASEAN countries —allowing operators in these markets to set up in other ASEAN markets — lenders would gain greater transparency around borrowers’ creditworthiness. Banks could expand their loan books and more institutional credit information on SMEs would be made available. The regional connection would make it easier for aspiring SMEs to tap capital markets and gain access to loans since that agency would be more conversant with local market dynamics.

Lower risk cost and concessions in funding. Greater efficiency and common standards will lead to improved decision-making, reduced risk, and lower operating costs. Better and more reliable credit information can allow banks to offer preferential interest rates based to high scoring customers.

Credibility. The absence of a credible regional credit rating agency may inhibit the growth of SMEs because their creditworthiness cannot be easily assessed. High performing SMEs aspiring to regional/global expansion may need to demonstrate creditworthiness in global deals/tenders. A good credit rating from a reliable regional body can help build SME reputations and help them win business, facilitating their expansion.

- For a successful regional integration to happen, there is a need for harmonising credit information across all markets in ASEAN The agency should be known for (i) independence (ii) transparency (iii) accurate ratings and high quality analysis (taking into account local market needs/sub segments/benchmarks and (iv) charge a nominal fee to encourage use.Before building a regional level agency it is important to adopt a pragmatic step by step approach to accomplish the end goal

Setting up and developing local credit rating agencies in each country where there are currently no agencies or adequate coverage such as Myanmar, Laos, Cambodia and Brunei. - Assist existing credit rating agencies to specialise in respective country’s key segments and markets and improve quality e.g. developing deep Micro segment, SME database by leveraging best practice within and outside the region.

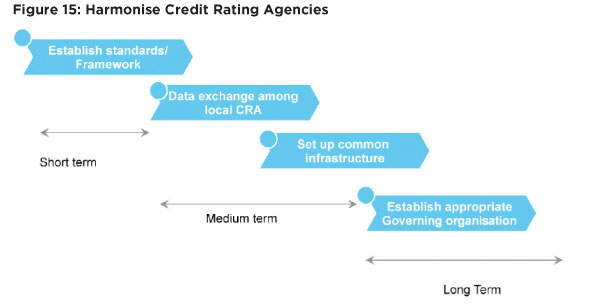

- Harmonise credit rating information across the region by setting up a common, preferably independent rating agency created through cooperation between ASEAN countries. The institution can help shape up a common standard of comparison across borders in terms of rating methodology, rating criteria, definitions, benchmarks and the overall rating process. As harmonisation is a complex process it has to be done in phases as illustrated below.

- Establish standards and framework. A central program office should be established to facilitate the initiative and provide governing guidelines. It is important to align differences in various rating-agency methods, tools, and practices towards creating common standards, while also allowing for local variations. Accounting disclosure standards, legal and regulatory elements, and base benchmarks should also be harmonised. Common standards, information architecture, and nomenclature should be established.

- Foster data exchange among local CRAs. Establish practices, processes, controls and channels of information sharing among different local CRAs in the region.

- Set up a common infrastructure. A formal regional-information location and common database need to be set up. Top regional banks and institutions with strong regional/global aspirations can collaborate to fund and establish a network. This network should leverage information from the credit rating agencies. The alliance can eventually be expanded with minimal government support on financing needs.

- Establish an appropriate governance organisation. There are many types of structures for a governance body. This can range from a new agency that will manage the common regional information, or a board comprised of representatives of local players.

1.3.6 Free Data Flow/Off-shoring

Banks rely on the free flow of data, standardised processes and modern technologies to ensure efficiency, scalability and quality of service. Regulators in the past have been reluctant to allow off-shoring and more importantly the cross-border transmission of client-sensitive data for reasons of security and privacy. While these concerns are valid there are equally valid reasons why allowing banks to structure their data and processing infrastructure on a regional level versus a multi-local set is important to support the eventual goal of a Financial Services regionalisation and liberalisation with in ASEAN. The key benefits being:

- Economies of scale (infrastructure, process efficiency and labour cost arbitrage)

- Risk management (e.g. understanding the bank’s exposure holistically at any point in time but also be able to make decisions quickly and quote best possible prices

- Compliance and control (e.g. ability to easily and in real time monitor and control key compliance processes e.g. KYC, AML etc.)

Some of the benefits around risk and compliance stated above are exactly in line with what the regulators have been struggling with, interms of being able to speed up and allow for regionalisation of banks. Such customer information sharing facilitates risk management in that banks can increasingly analyse customer and third party payment patterns cross border, facilitating anti-money laundering and anti-terrorist financing measures internally. This avoids unhelpful situations where suspicious transaction reports are filed in one jurisdiction or accounts closed, while these are continued in another jurisdiction without knowledge of the account activity in the first jurisdiction.

So this particular topic on allowing for a centralised and regionalised operating model has systemic benefits.There are multiple examples of processes that can be offshored to create cost efficiencies. These include call centers, back office centers, and IT infrastructure centers.

1.3.6.2 The key benefits of off-shoring and free data flow

- Off-shoring non-critical processes promote economies of scales and competency building, benefits that translate into lower cost of service and improved quality. It can also help foster the development of local modules that meet specific market needs.

- Centralised processes and strong off-shore capabilities can promote product innovation and allow banks to forge alliances to leverage existing infrastructure and build products using such strong infrastructure (e.g. Trade platform).

There are pragmatic measures that can greatly help reduce the real and perceived risks and aid the banks to pursue an effective regionalisation strategy, which will not only benefit the bank and customers but also aid the regulator in managing risks more effectively.

- Alignment or ratification of data protection laws within ASEAN: This can either be done at a regional level or a bi-lateral level or one could even look at examples of other developed economies. UK’s FSA for example in its outsourcing regulation had provided for off shoring to a destination where the data protection laws exist and are comparable. It also requests for framework where it can be assured that reasonable access and audit of the off shored infrastructure can be conducted by FSA principle. Such regulation has been behind the success of offshoring and centralisation of infrastructure of many banks in emerging economies such as India.As a next step consumer protection can also be explored contextually with transparency and consumer choice as a key principle. For example, exploring alternative ways of obtaining, respecting and enforcing for the collection, processing and use of personal data (appropriately worded consent clauses in standard on-boarding terms) and informing the customer on who has their data, why and how it will be used can enable customer to exercise an informed choice and such transparency is over and above just consent.

- Alignment and/or standardisation of prudential operational guidelines on information systems and operations: This can be achieved through professional certification on global standards on security such as ISO 27001/27002 for the offshore facilities. This will enforce adherence to minimum set of criteria for having their regional technology and processing infrastructure certified for a pan ASEAN presence. This might even have second order benefits where “Pan-ASEAN” banks might seek to locate some of their IT infrastructure to a lower cost location within the ASEAN as well.

- Enabling accessibility: This is crucial element to enable any kind of cross border operation. Reasonable, timely and un-fettered access to regulators for inspection and audit. This can be implemented via special onetime visas (where this is not already possible) that are available for regulatory authorities to be able to visit and inspect premises that are based in other geographies. This is also important to apply to bank employees should they need to access these infrastructures to remedy critical issues.These practical measures can address some of the concerns regulators have around having data and processing outside their jurisdictional boundaries and in the process reaping benefits on risk and compliance over and above significant customer benefits. A healthy dialogue on the types of data, disclosure norms, and compliance among banks and regulators is required.

1.3.7 Standardisation of Nomenclature, Documentation, and Common Infrastructure

There are pragmatic measures that can greatly help reduce the real and perceived risks and aid the banks to pursue an effective regionalisation strategy, which will not only benefit the bank and customers but also aid the regulator in managing risks more effectively.

1.3.7.1 Overview

One of the key success elements of any banking architecture or framework is the standardisation of nomenclature. Since having varied definitions of terms can create widespread misunderstandings, products, contract terms, banking terminologies, all must be well defined to ensure everyone is “speaking the same language.” In Europe ECB defines a reporting structure for products and defines classifications and publishes glossary of all terminology periodically.

Likewise, it is important to standardise documentation, forms, and information requirements for basic products. Regulators must also encourage banks to standardise processes that are routine in nature such as KYC, account opening, account closing, and scan factory as well as common platforms, such as payments. This can be a pan-ASEAN initiative based on alliances and cooperation among banks.

Europe’s Single Euro Payments Area (SEPA) offers a good example. It provides common standards, faster settlement, and simplified processing. Consumers can rely on a single set of euro payment instruments that together cover 33 countries with one bank account, one bank card, one SEPA Credit Transfer (SCT), and one SEPA Direct Debit (SDD). Successful implementation will require alliances to build infrastructure, access to a common talent pool, and support from every country.

1.3.7.2 Benefits of standardisation

Lower fees/cost to customer. Standardisation is one of the main drivers of economies of scale. It also lowers operational risk. In addition, a common infrastructure can help pool investments which lower costs while also facilitating multi-stakeholder integration such as B2G, B2B, G2C, and B2C effectively.

Quicker and Efficient processes. Consistent, clear documentation and nomenclature makes it easier for customers to complete forms and for banks to improve response times and accuracy.

- Agree which banking terminology to standardise, define a nomenclature and build common regional information architecture for continuous improvement.

- Simplify forms and define common types of documentation requirements for customers.

- Identify key processes across banks and set up a shared services alliance among banks to scale operations.

- Create a plan for region-wide payment infrastructure to facilitate more seamless cross- border payment.

Standardise disclosure standards

1.4 Conclusion

It is always difficult to determine the degree of openness of an economy or integration of a region. It is even harder to align different stakeholders on the “right” amount of openness and integration. Especially in recent years – during the financial crisis – many regional efforts across the globe have stumbled when economic growth has been challenged and hence their rationale has been questioned. However, when it comes to Europe some might argue that regional growth has stumbled because of too much integration whereas others argue that it has happened because of not enough integration.

In any case, ASEAN has chosen a unique approach to regional collaboration and integration. The ASEAN Economic Community (AEC 2015) vision actually differs in quite some ways from the EU-style integration. More so, it has an opportunity to develop and refine it further in a way that will suit the region’s requirements, learning from experiences made elsewhere as well as its own experiences in the past during the Asian Financial Crisis.

Policymakers will need to evaluate a variety of factors, foremost of which should be the type of structure that will best benefit the customer. In making those decisions, they will need to weigh complex issues stemming from the region’s economic diversity, such as volatility in capital flows and differential economic growth rates, when determining the pace and extent of the desired integration. Finding the right balance will depend on the size of the ASEAN countries, the needs of the local market, the efficiency of their underlying infrastructure and access to financial services, and the strength and maturity of the legal and regulatory environment.

Creating a stable financial system immune against systemic risks or contagion effects is of tremendous value to the society at large. However, too stringent regulation also comes at a price – providing better access to better financial services at lower cost is important to reap the full benefits of ASEAN 2015, spur economic growth and increase the wealth of nations. From our discussions with some of the leading banks in the region we believe that in some markets domestic banks feel rightfully strong enough to weather more intense competition and customers would benefit from this competition. The emergence of regional ASEAN banks and pan-ASEAN alliances, being able to capture the value from operating on a regional platform, would create the right conduits to facilitate cross-border economic activity. And reducing information asymmetry on the lending side should help to increase the overall lending capacity in the market, especially as some economies like Indonesia are hitting system wide Loan-to-Deposit ratios of 100%.

The stark economic and political differences between the 10 ASEAN members are a recognised fact. For some of the more advanced markets the question is if the additional customer value gained by more market liberalisation and reciprocal market access for qualified institutions would not outweigh the currently perceived benefits of a more restrictive regulatory stance. Having such a debate at a regional level, including all stakeholders and with a broadly defined “customer value” as the guiding metric could be an important step forward.

![]()

RELATED REPORTS

- AN ANALYSIS OF THE ASEAN PRIORITIES ON IMPROVING GOOD GOVERNANCE

- LIFTING-THE-BARRIER REPORT 2013 CAPITAL MARKETS

- LIFTING-THE-BARRIER REPORT 2014 FINANCIAL SERVICES & CAPITAL MARKETS

- LIFTING-THE-BARRIER REPORT 2015 FINANCIAL SERVICES & CAPITAL MARKETS