Economic Snapshot: ASEAN Focus Jan 2017 | Malaysia

Published on 24 January 2017

by Dr. Arup Raha, Chief Economist, CIMB ASEAN Research Institute

The economy has weathered several external headwinds over the last few years and growth has slowed. But with exchange rate flexibility and well functioning financial markets, macro-stability has been maintained. This may be the year where it also finds stabilization in its growth rate or perhaps even a modest increase over the 4.2% pace in 2016. Much will depend on the external sector, which while shrinking in relative terms, still remains crucial to Malaysia’s fortunes. Inflationary pressures, though modestly greater on firming commodity prices, are not an area of concern and, under usual circumstances, the bias for policy rates would have been to the downside. However, the firmer US rates outlook and recent pressure on the MYR may have ended the rate cutting cycle. The MYR has been volatile and in 2017 I expect it to move largely in line with regional currencies, with the dollar index and the RMB playing meaningful roles in determining its value.

Growth – stability first

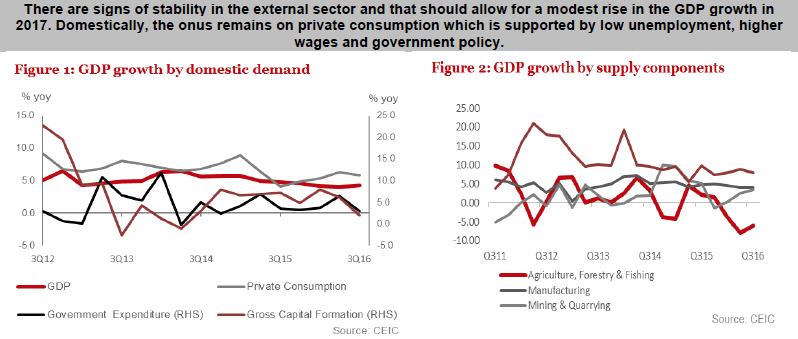

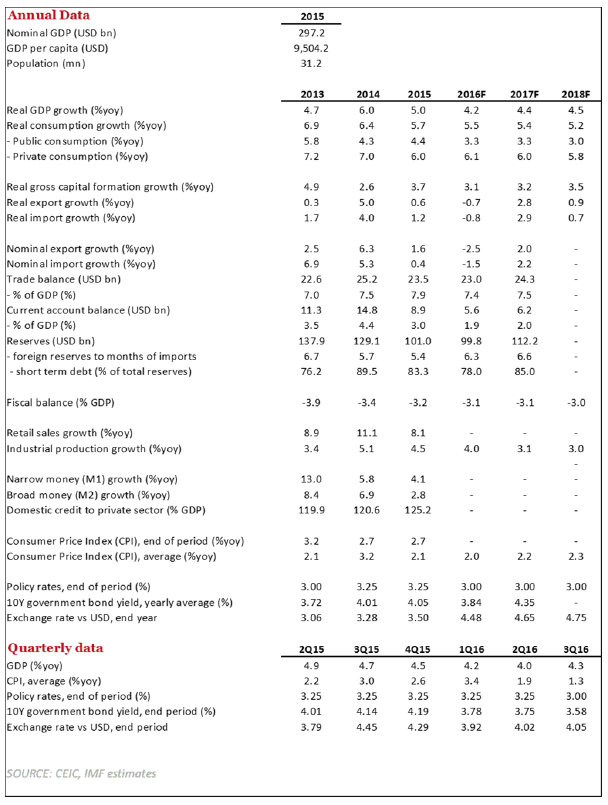

- There are more signs of life in the economy with 3Q16 GDP growth at 4.3% a small uptick from 4% growth in 2Q. For 2016, I expect GDP to grow by 4.2%, a continued decline from 5% growth in 2015 and 6% growth in 2014.

- Private consumption has helped cushion the downturn, growing at 6.4% in Q3 and 6.2% in Q2. It is being supported by a low unemployment rate, an increase in the minimum wage in July 2016, and support from the government. I expect a similar trend to continue in 2017, especially as the 2017 budget has provisions to support the lower income parts of society.

- The composition of public investment is changing with a greater emphasis on transport and infrastructure being offset by a decline in capacity expansion in the oil and gas sector. Private investment is likely to be restrained as sentiment has suffered. Moreover, as is typical in most countries, I expect large capital commitment to be held back until after the elections.

The external sector – the turnaround factor but not without risk

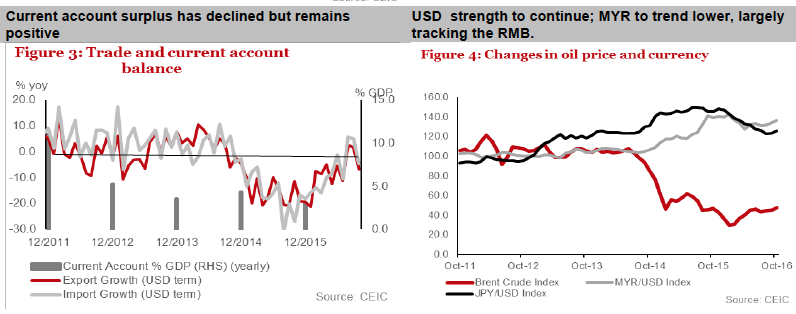

- In US dollar terms, export growth has been negative, down 6.2% in the first 11 months of 2106. In volume terms they have done better, being close to flat implying a deterioration in the terms of trade (export-to-import prices). This decline — 1.9% (ytd until November) – negatively affects real income growth.

- Over the first 11 months of 2016 imports did better than exports, but not much, down 5.2% in USD terms. For 2016, the current account should narrow but is still expected to be in surplus at 1.9% of GDP. In 2017, with better export and import growth rates, the surplus should be of a similar size.

- Exports seem to have stabilized in November registering a large increase of 7.8% yoy in MYR terms; year-to-date exports were almost flat rising just 0.2%. While it is tempting to get excited about the November numbers, a few words of caution are in order. First, the October numbers were poor so there may simply be some catch up. Second, exports to China were strong at 12% yoy and some of this strength came from commodity exports which are not being matched by an increase in Chinese domestic demand. As such, some of this increase reflects speculative demand and may not continue. Third, commodity prices have been firm recently, undoubtedly helping export numbers. Again, this too may not continue as currently commodity prices and the US dollar are moving together while there is typically a negative correlation.

- In my view, the external outlook will be crucial to determine Malaysia’s growth trajectory in 2017. In my base case, there is modest growth of both exports and imports, to some extent due to a better global economy but also because of the low base of comparison. The external sector also poses the greatest risk given the uncertainty of policy in the US and developments in China. Implicit also in a more constructive external sector outlook is firmer commodity prices. Despite the downturn in exports, a current account surplus of MYR6.9 billion (1.2% of GNI) for 1H16 has remained, as import growth has been almost as poor. The decline in import growth has not been due to soft domestic demand but due to reduced supply chain requirements for exports. The current account surplus has provided a buffer against external shocks and allowed for some policy flexibility.

Inflation has picked up but is not a cause for concern

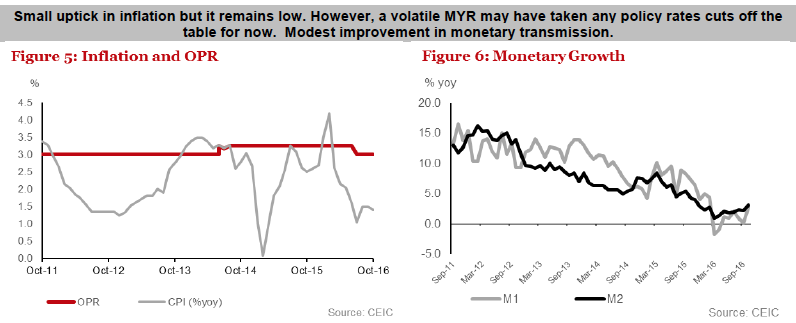

- After peaking in February, inflation followed a downward path until June, until a recent uptick to 1.8% yoy in November. The rise in inflation has largely come from a rise in commodity prices, while the diminishing impact of the GST has worked in the opposite direction. I expect inflation to come in at around 2% for 2016 and between 2-2.5% in 2017; numbers that are not high enough to elicit a policy response.

Rates on hold; weaker currency

- While one rate cut is possible next year, the likelihood has gone down significantly. For that to happen, it would require much greater stability in financial markets and the currency in particular. With the new US administration, the 19th People’s Party Congress in China, and the possibility of elections in Malaysia, markets are likely to be more skittish than usual, making a rate cut a difficult decision.

- Externally-driven volatility is likely to affect how the currency behaves. As argued in the “Currency” section of this report, more likely than not, the onus of adjustment to external developments will fall mainly on the Ringgit as the other shock absorbers, such as policy rates or reserves, do not have much space. I expect the MYR to end the year at around 4.65 to the USD, based largely on my belief of USD strength and RMB weakness.

Risks and Other Issues

- On the positive side, it appears that fiscal consolidation has stayed on track. The deficit was above target in 1H16 but consolidation in 2H makes it likely that the deficit will meet its 3.1% of GDP target. Further consolidation to 3% in 2017 will require operational discipline. Further diversification of the export base may be needed down the line.

- The economy is still heavily reliant on trade even though trade as a percent of GDP has declined from close to 200% to less than 140% over the last decade. This change, coupled with the end of the commodity boom, means that the growth strategy needs to

reconsidered and greater investment made in productivity-enhancing infrastructure and human capital. - The risks are mainly external. Internally, there is a belief that elections will be held in Malaysia in 2017. That creates uncertainty in the decision making of the private sector and could possibly provide a worse growth outcome than I expect. A further hit could come to growth if oil-related revenues disappoint and therefore force the government’s hand into curtailing operating expenditures.

![]()