Economic Snapshot: ASEAN Focus Jan 2017 | Thailand

Published on 27 January 2017

by Dr. Arup Raha, Chief Economist, CIMB ASEAN Research Institute

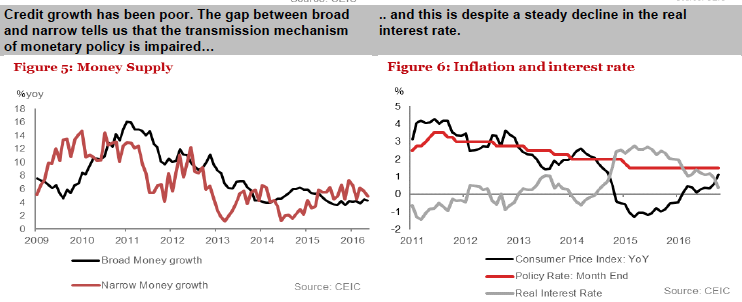

A modest recovery is underway in Thailand. The economy is expected to grow by 3.1% in 2016 after growing by 2.8% in 2015. In 2017, my expectation is for a further increase to 3.3% growth. The recovery is not yet firm as various components of growth slowed in 3Q16 for an aggregate clip of 3.2% compared with a 3.5% rate in Q2. Moreover, with sentiment being negatively affected by King Bhumibol’s passing, 4Q growth is unlikely to be much better. Growth is not yet broad-based as private investment remains soft as do exports. Nevertheless, agricultural incomes are rising, tourism is doing well, and the government is supportive in its fiscal plans. Public investment is likely to be a key driver of growth in 2017 and beyond. On the supply side, services, mainly tourism receipts are strong but manufacturing is sluggish. Inflation remains soft at less than 1% despite a recent rise and real rates are low; the policy rate has held steady at 1.5% since April 2015 and I do not expect a change any time soon

even with rising US rates. A large current account surplus has allowed the THB to be less volatile than most regional currencies and I expect it to continue to be resilient to external shocks. In 2017, I expect it to move in line with the Chinese RMB to maintain trade competitiveness.

Growth – a slow recovery that needs to broaden out

- The economy grew by 3.2% in 3Q16, a modest deceleration from the 3.5% clip in 2Q15. The slowdown has quite broad with fiscal expenditure down 2.4% yoy in 3Q16, with both public consumption and investment slowing. Both should recover in 2017 as expenditure in 2016 was front loaded.

- Private consumption also slowed but the outlook is more positive with agricultural incomes recovering after a prolonged drought. There is however a countervailing force on consumption as household debt is high and there is a need to deleverage

- Credit is sluggish — 3Q lending growth was 2.3% yoy – and growth for the year is likely to be between 2-3%, less than the 4.3% pace of 2015. Lending to corporates grew by just 1.1% and points to a continued sluggishness in manufacturing. And with capacity utilization rates at around 67.7%, it doesn’t augur well for private investment either. However, note that three sectors have high capacity utilization — IC and semiconductors; autos and petroleum – so there could be pockets of improvement.

- Fiscal policy and implementation will be crucial. There is fiscal space as public debt to GDP stood at about 43%, versus a self-imposed ceiling of 60%. And, to their credit, the government has been making the most of this space with a focus on building infrastructure. The deficit in FY16 is expected at just below 3% of GDP. However, according to the World Bank, disbursements on the capital side where at 66.8% of the budget versus a target of 87% set in September 2015. If large infrastructure projects, such as the dual track rail, are successfully implemented in 2017, it could potentially crowd in private investment.

- Although the government consumption slowed from 13.5% (Q2) to 3.1%(Q3) following the tapering off of the election related spending, we expect it to pick up in 2017 as the proposed budget for 2017 is 11.6% higher the previous one. The government outlays should provide momentum to the economy in next 2 years.

- On the supply side of the economy, manufacturing remains weak but agriculture is recovering after a prolonged drought. In 3Q16, it grew by 0.9% after several quarters of contraction. Tourism remains an area of strength. In 3Q16, arrivals grew by 13.1% while receipts increased by 17.1%, mainly due to Chinese visitors. Tourism is now 13% of the economy and likely to play an increasingly large role.

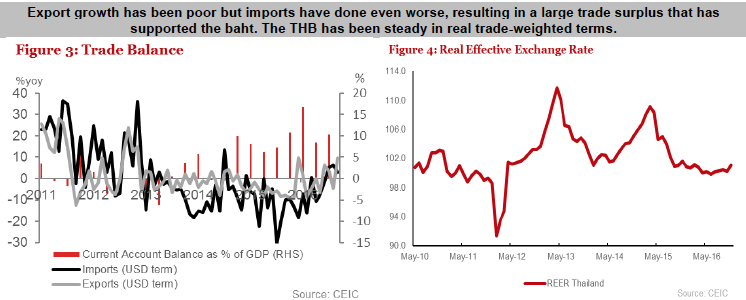

A large current account surplus, mainly due to good tourism receipts and poor imports

- The robust tourism numbers have helped add to a current account surplus that is already being boosted by a rising trade balance. Exports declined by 5.6% in 2015 but imports fell by 10.6%, resulting in a current account surplus of 8.1% of GDP. A similar trend has continued in 2016, with exports down 0.5% in the first 11 months, but imports down by 6%.

- In 2017, I expect both to show positive, though modest growth. The trade balance should stay strong and with the service and income account likely to have a strong showing, the current account should stay in surplus close to 10% of GDP.

- The large surplus is expected to persist even though the outlook for exports is not constructive. I expect exports to shrink 0.5% in 2016 in US dollar terms. However, with weak domestic demand, imports are also likely to fall and the current account is expected to be about 10% of GDP in surplus.

Monetary policy and the currency

- The large current account surplus, low inflation, and healthy reserves have given Thailand a fair amount of space in the conduct of monetary policy. However, policy rates have been steady at 1.5% since April 2015, largely because credit growth did not seem particularly sensitive to changes in the interest rate. I expect that, barring exceptional regional volatility, policy rates will stay unchanged even as US rates go up.

- The THB is well supported, but is likely to weaken in tandem with regional currencies, more to maintain Thailand’s competitiveness in regional supply chains than anything else.

Risk and other Issues

- There is politics, both domestic and international. With elections due, and now with the date uncertain, investors may hold back to see what direction policymakers go in. On the external side, there is uncertainty regarding the policies of the incoming US administration.

- The outlook for 2017 and beyond depends crucially on implementing fiscal plans, especially on building infrastructure. However, disbursement rates had typically fallen short for capital expenditure and need to be stepped up.

- At the time of writing, here have been severe floods in the southern part of the country, risking some damage to certain crops and tourism. It may result in a moderated growth in 1Q17.

- The economy seems to be settling into a low trend rate of growth. After averaging 6% growth for 30 years until the crisis in 1997, it appears that the economy is now settling in for a near 3% growth rate. As World Bank has pointed out, the economy may be reaching the limits of the old export and manufacturing led growth model and it may be imperative to focus on services as a driver of growth. With 40% of the work force

employed there, the returns are likely to be high and could potentially shift Thailand’s trend rate

![]()