Economic Snapshot: ASEAN Focus December 2017 | Indonesia

Published on 20 December 2017

by Lim Yee Ping & Michelle Chia, Economists, CIMB Equities & Economic Research

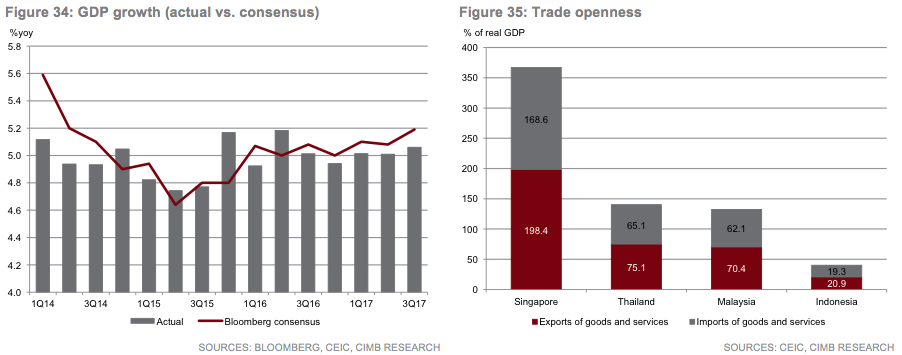

INDONESIA: Firmer recovery in GDP growth

Reforms and monetary policy tightening following the double whammy of a taper tantrum in 2013 and large declines in commodity prices during 2H14-2016 weakened economic growth to the 5% range in 2014-2016 (vs. +6% yoy in 2010-2013). As some policies have been unwound on the back of macroeconomic resilience, a gradual recovery in private consumption could be in sight amid firmer commodity prices, higher minimum wage growth, low inflation environment and falling lending rates. Investment growth shall continue to ride on the improved investment climate and infrastructure spending. Hence, the economy could experience stronger growth in 2018 (+5.3% yoy vs. +5.1% yoy in 2017).

Overview of GDP growth in 2017

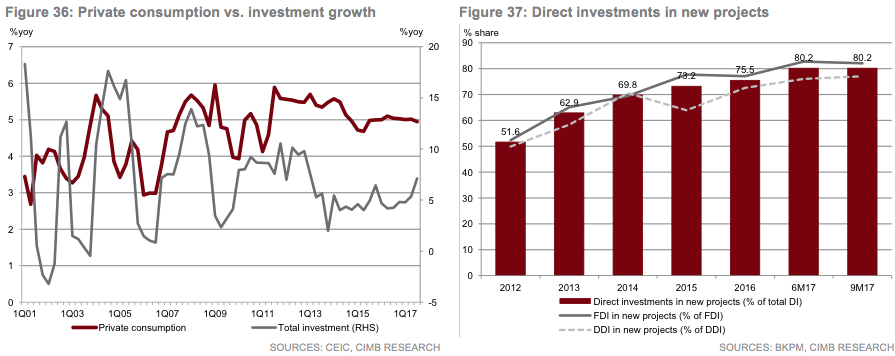

Indonesia’s GDP growth has largely underperformed expectations YTD (+5.0% yoy in 9M17) on the back of sluggish private consumption (accounting for 55% of the economy), mitigating the improvement in investment and export performance. The positive spillover from growing external demand to domestic consumption in Indonesia has been limited compared to its regional peers, which recorded upside surprises to growth. This was due to the country’s relatively lower trade openness compared to its regional peers as well as higher dependence on commodities, implying that the direction of commodity prices exert greater influence on its economy and trade performance than the upturn in technology and manufactured goods cycles.

Private consumption: gradual improvement

Private consumption has been the key laggard in recent years impeding the progress of growth recovery. Household purchasing power was eroded in 2013-2015 following drastic policy changes that aimed to restore macroeconomic stability and fiscal overhang concerns. Changes, such as aggressive hikes in policy rates (+175bp in Jun-Nov 2013), tightening macroprudential measures and energy subsidy overhauls, coupled with exogenous declines in commodity prices since 2H14 which dampened household incomes, eventually led to a weakening in private consumption growth to the 5% range (vs. +5.5% yoy in 3Q11-2Q14).

As some of the policies (i.e. policy rate, macroprudential measures) have been unwound since 2016, and this may support private consumption in 2018 (+5.2% yoy vs. +5.0% yoy in 2017). Disposable income will likely improve further on the back of stronger minimum wage growth (+8.7% yoy vs. +7.2% yoy in 2017), a stable commodity price outlook and social disbursements, i.e. more low-income households (10m in 2018 vs. 6m in 2017) receiving the government’s conditional cash transfers. Moreover, the household desire to save may take a breather given that deposit growth has reverted back to its 5-year average, indicating improvements in balance sheet buffer. The Asian Games 2018 may also lend a supporting hand to consumption growth, especially among middle-income households where consumption patterns have arguably shifted towards leisure.

Households will enjoy a low inflation environment for the third straight year (+3.7% yoy in 2018 vs. +3.8% yoy in 2017). While the possibility of administered price increases has been reinstated amid a stronger oil price outlook, the adjustment may likely be one of the mildest compared to previous hikes.

Investment: riding on policy reforms and infrastructure

Investment growth rose to +7.1% yoy in 3Q17, the strongest since 1Q13, supported by both foreign direct investment (FDI) and domestic direct investment (DDI). Moreover, an increasingly higher proportion of investment realisation came from new projects, arguably reflecting greater investor confidence amid an improving investment climate and a sovereign rating upgrade by S&P.

Expect investment to continue growing in 2018 (+5.6% yoy vs. +5.7% yoy in 2017). The government’s emphasis on off-budget financing options (so-called ‘creative financing’), i.e. capital-raising by state-owned enterprises (SOEs) and Non-Government Budget Investment Financing (PINA), continues to support infrastructure spending. Investments in sectors such as tourism, e-commerce and logistics could be attractive to foreign investors given the revision in negative investment lists, which opened up these sectors to foreign investments. Nevertheless, concerns over policy continuity and political risks, i.e. regional and presidential elections in 2018/2019, could slow implementation and deter new investment or expansion in extractive sectors, such as O&G and mining.

Government tax revenue remains a key downside risk

The government has set a fiscal deficit target of 2.2% of GDP under the State Budget 2018. If this materialises, the deficit will be the smallest in four years. Nonetheless, a shortfall in tax revenue collection remains the key downside risk. Tax revenue collection only reached 78% of the target in 11M17 despite a Tax Amnesty programme and higher O&G revenue receipts. Assuming a realisation rate of 90% for 2018 (vs. 88% in 2013-2016), fiscal deficits could breach the 3% legal limit if it is not matched by a corresponding cut in expenditure.

Hence, the change in tone on administered price increases amid rising oil prices (US$59/bbl in Nov 2017 vs. government assumption of US$48/bbl) is an inevitable move to mitigate the fiscal burden. Although the burden of the Premium gasoline subsidy lies with Pertamina, it indirectly affects government revenue through O&G income tax and Pertamina’s dividend payouts to the government.

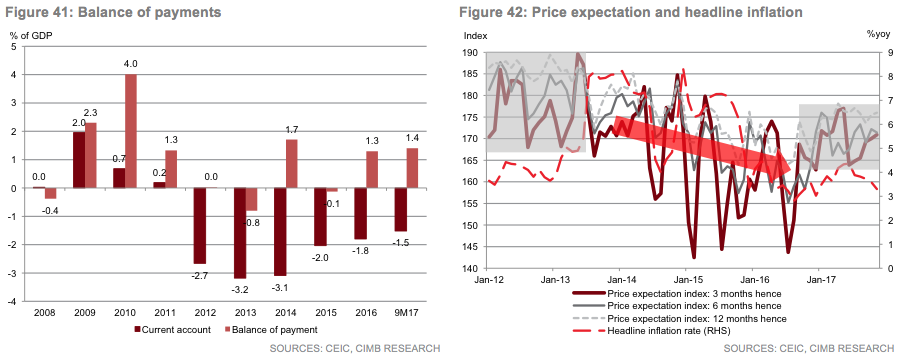

Meanwhile, the implementation of fiscal reforms, such as the electronic tax filing and participation in Automatic Exchange of Information (AEOI), could help to improve tax collection capability in the longer term and address the twin deficit concerns. Fiscal deficits have been on the rise (-2.4% of GDP in 2013-2016 vs. -1.0% of GDP in 2003-2012) and rising foreign holding of government securities (39% as of Nov 2017) has caused primary income deficits under the current account (CA) to rise.

FDI to provide stable financing to current account deficits

On the back of firmer commodity prices, global growth outlook and higher travel receipts, expect the current account deficit (CAD) to remain manageable in 2018 (-1.8% of GDP vs. -1.6% of GDP in 2017)

Deregulation in the investment space has somewhat improved the prospect of stable long-term financing for the country. Greater ease of doing business and FDI liberalisation have pushed net direct investments up from 1.3% of GDP in 2013 to 1.9% in 9M17. That said, current account deficits (CAD) in the past five quarters have been financed by the more stable direct investment inflows. This partly reduced external financing risks from volatile portfolio flows, which could be susceptible to global monetary policy and market sentiment. The FDI liberalisation in some sectors (i.e. tourism, logistics, transport) could benefit CA in the longer term through higher travel receipts and lower logistics costs.

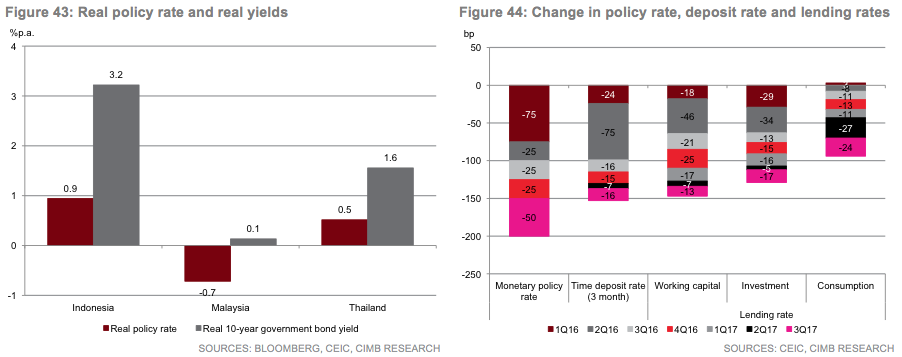

Monetary policy stance to remain neutral

Although more countries are expected to join the monetary policy normalisation camp in 2018, Bank Indonesia (BI), which recently lowered its rate twice amid disappointing growth performance, is unlikely to reverse policy rate decision given that Indonesia’s real policy rate and real bond yields remain attractive compared to its regional peers’, thanks to a waning inflation rate.

The policy mix implemented by BI and the government since 2013, although painful and come with the cost of lower growth, has nonetheless strengthened the resilience of the economy. Inflation is no longer soaring and volatile, CAD as % of GDP declined and international reserves increased (US$126.0bn/8.4 months of imports as of Nov 2017 vs. US$100.2bn/7.1 months of imports as of Nov 2015).

The extended period of price stability has guided inflation expectations lower with smaller fluctuations, as reflected in the price expectation indices for 3-12 months ahead, implying that changes in Indonesia’s monetary policy stance will likely be less volatile compared to the past, enhancing its central bank’s credibility. Hence, the chances of abrupt and volatile capital outflows, such as those seen in 2013, are low. Expect the central bank to keep the policy rate at 4.25% in 2018.

Appendix: Indonesia

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()