Economic Snapshot: ASEAN Focus December 2017 | Singapore

Originally published on 20 December 2017

by Michelle Chia & Lim Yee Ping, Economists, CIMB Equities & Economic Research

SINGAPORE: Canary in the coalmine to continue singing

Singapore’s GDP growth is projected to accelerate to 3.6% in 2018, from 3.5% in 2017, aided by a broadening out of gains from the external sector and manufacturing, to households and services. The government may increase the Goods and Services Tax in the upcoming Budget 2018 to fund infrastructure upgrades and higher social spending. Expect the improving growth picture, uptick in core inflation and monetary policy tightening in advanced economies to nudge the Monetary Authority of Singapore into tightening policy by strengthening the S$NEER in Apr 2018. (Nominal Effective Exchange Rate) in April 2018.

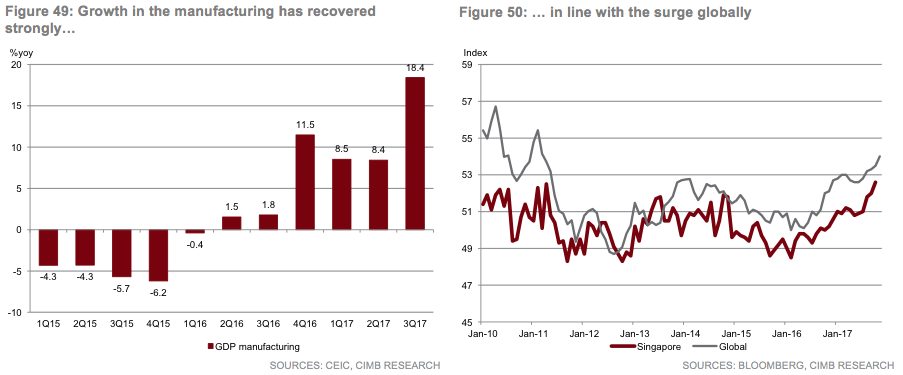

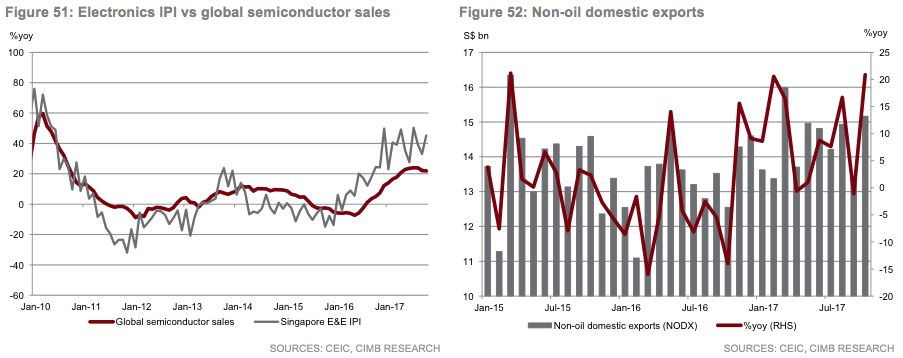

Growth rekindled by external demand

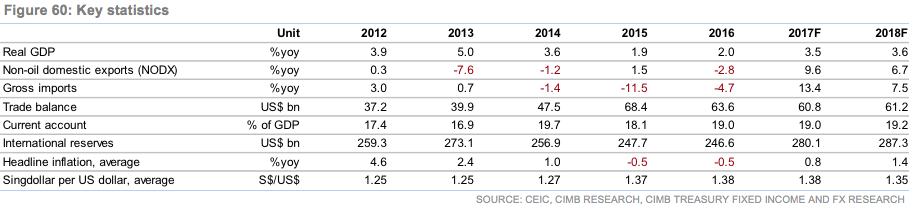

The cyclical recovery in global trade, and electronics demand in particular, provided an injection of momentum into Singapore’s bellwether economy in 2017. The official forecast had been revised higher, from an earlier range of 2.0%-3.0% to 3.0%-3.5%, after the strong set of numbers emerging from the manufacturing and export-driven sectors. Expect Singapore’s economy to record a GDP growth of 3.5% in 2017, shrugging off the lacklustre 2.0% expansion in 2016.

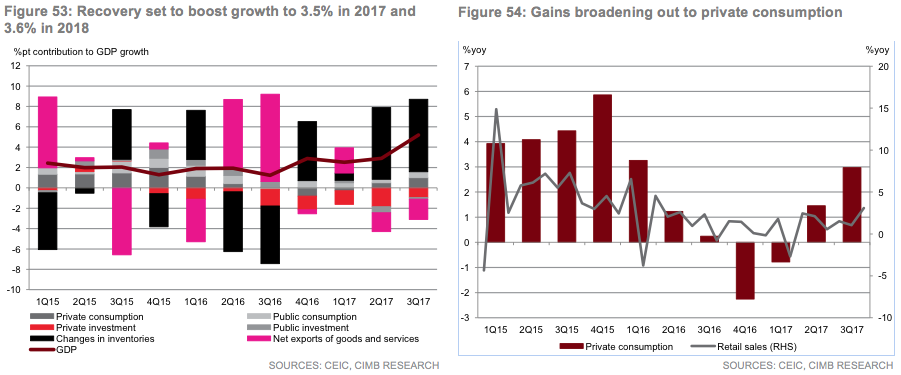

GDP growth to quicken marginally to 3.6% in 2018

The prognosis for 2018 appears positive, growth in Singapore is expected to broaden out from the external sector to the domestic economy. The government is forecasting a GDP growth of 1.5% to 3.5% in 2018, which may prove to be conservative. The more optimistic scenario of 3.6% expansion in 2018 takes the stand that domestic demand will contribute more strongly to headline growth (+3.9% in 2018 vs. -0.2% in 2017). Risks to the outlook include disruptions to the positive trade cycle, tighter financial conditions due to more restrictive global monetary policy, geopolitical uncertainty and a sudden loss of momentum in the economies of the US and China.

Positive spillovers to domestic economy

Labour market conditions appear to be turning around, as the pace of layoffs has slowed. The overall unemployment rate was stable at 3.2% in Sep, while the unemployment rate for Singaporeans fell to 3.2% in Sep, from 3.3% in Jun and 3.5% in Mar. Improvements in business conditions this year should cascade down to higher household income growth and boost consumer spending in the year ahead. Expect the subdued investment environment to turn more positive in 2018 (+4.4% vs. -4.9% in 2017), with both private and public sector outlays on the rise.

Total trade growth is expected to moderate next year, as capital spending growth slows in China and following high base set in 2017. In tandem, the export-driven segments of the manufacturing sector should expand more modestly (+4.7% in 2018 vs. +9.2% in 2017). Nonetheless, expect the shortfall to be offset by expansion in construction (+2.5% in 2018 vs. -4.6% in 2017) and services (+3.4% in 2018 vs. +3.1% in 2017).

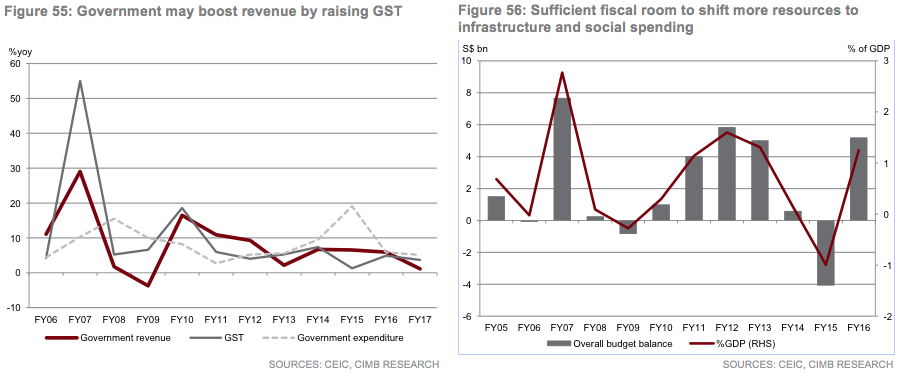

A potential GST hike in upcoming budget?

In Nov, Prime Minister Lee Hsien Loong suggested that taxes are set to rise to fund higher infrastructure investments and social spending in the coming years to cope with ageing demographics. If such a move is being considered in Budget 2018, to move the needle, the government would look to tap the largest sources of tax revenue: corporate income tax (22.9%), individual income tax (15.6%), goods and services tax (14.0%), property tax (6.2%) and stamp duties (6.0%). Of the above, GST presents the most efficient option, though it may be politically challenging to implement. More than a decade has lapsed since the GST was last revised in Jul 2007, with an upward adjustment from 5% to the current 7%. Each 1% pt increase in the GST would yield additional revenue of about S$1.6bn based on the expected GST collection of S$11bn in 2017 and add fiscal room to the tune of 0.4% of GDP. Any hike in the GST would likely be coupled with measures to help households manage an increase in the cost of living. The government has also stated that it is exploring ways to raise revenue collection from other sources, such as e-commerce, to broaden the tax base.

Inflation risks lie to the upside

The brighter outlook for domestic demand is expected to translate into a mild uptick in demand-driven inflation in 2018. Imported inflation could increase moderately due to rising global demand and an uptick in commodity prices, feeding into higher domestic food and energy prices. The MAS core inflation, which strips out accommodation and car prices, averaged 1.5% in 10M17, as economy-wide cost pressures remain relatively restrained. Expect headline inflation to accelerate to 1.4% in 2018 from 0.8% in 2017, but upside risks lie in the potential implementation of a GST hike in Budget 2018.

On the cusp of monetary policy normalisation

The Monetary Authority of Singapore (MAS) may be compelled to normalise monetary policy in 2018, to stay ahead of the curve as growth prospects improve and the core inflation outlook draws nearer to the policy target of slightly below 2%. Expect MAS to shift the policy band of the S$ nominal effective exchange rate (S$NEER) at its next review in Apr 2018, allowing the currency to appreciate via a steepening of the slope, but keeping the width and centre of the band unchanged. MAS had last reduced the slope of appreciation in the S$NEER in Oct 2015 and Apr 2016, as inflation slipped below the policy target.

Appendix: Singapore

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute. The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.

![]()