LIFTING-THE-BARRIERS REPORT 2013 | HEALTHCARE

Published date: November 2013

TABLE OF CONTENT

(Click any topic to read the related section)

- Executive Summary

- Methodology

- Healthcare Lifting The Barriers Roundtable Observations – notes

- Recommendation and NAF Feedback

- Challenges identified

- Current State of AEC and areas of additional focus

- ASEAN countries overview

Executive Summary

Overview

Healthcare is one of the 12 priority sectors identified to drive ASEAN integration. Regional cooperation in healthcare issues is crucial due to the disparity of healthcare sectors among ASEAN countries and the emergence of highly infectious diseases that can easily spread around the region.

The content for this Lifting-The-Barriers Paper has been developed through research and industry roundtable discussions to provide a more holistic view of the challenges and possible solutions for the healthcare industry in ASEAN leading up to ASEAN Economic Community (AEC) 2015.

The current state of play for the individual members of ASEAN and the progress achieved to meet the objectives of the AEC are lagging behind the timelines projected.

Contributing to this is the very same variability between countries that makes ASEAN such a diverse community and culturally rich environment – not everyone is at the same state, policies and legislation are widely different, fiscal flexibility is available to only a few countries and the barriers for export or entry for healthcare provision are inconsistent and uncoordinated.

True integration for all will be unlikely, and indeed, the vision for what integration in ASEAN entails should be the topic for a strategic paper, looking at benefits as well as pragmatic approaches for providing good affordable healthcare to all in ASEAN, both within and across borders in a timeframe that aligns with each countries evolutionary journey.

There are some identified challenges that each country faces, which not only impede progress within a country but also the ability of that country to provide or receive support to theirs or other nation’s healthcare infrastructures – these are broadly categorised into policy constraints, economic challenges, labour limitations and socio-cultural expectations.

However, in the interim, as we progress to 2015, focused efforts on some areas of commonality will help drive integration and equality forward. Through the Network ASEAN Forum Lifting-The-Barrier Roundtables a number of findings and recommendations have been suggested that are low hanging fruit and readily achievable to support the creation of an AEC healthcare landscape.

Recommended

- A Pan-ASEAN medications approval process.

- Easing the requirements allowing medical travel.

- More recognition of neighbouring country’s clinical training and qualifications.

- Expedite existing AEC initiatives, such as obligating mutual recognition agreements.

Suggested

- Support and legislate for privately managed professional training.

- Providing capability and expertise from developed countries to support the less developed ecosystem.

- Provisionally ensure that delivery of care needs internally are met, then surplus can help deliver care externally.

- Form collaborative working groups to develop wellness strategies between healthcare groups and industries aligned to health and well-being – food and beverage etc.

Additional initiatives needed for an integrated healthcare sector include; harmonising standards, making further widespread mutual recognition agreements (MRA), creating joint post marketing surveillance mechanisms and establishment of universal healthcare currencies and cross border reciprocal basic healthcare provision agreements.

Methodology

Overview

This Healthcare Lifting-The-Barriers (LTB) Report has been generated through three distinct inputs.

Part 1 – Preliminary Paper

Primary and Secondary Research was carried out prior to the Lifting the Barriers Roundtable event at the Network ASEAN Forum, Singapore in August 2013.

Primary and Secondary research partners included Accenture and IHH Berhad Healthcare, supported by CIMB ASEAN Research Institute (CARI).

For the Preliminary Paper, there was a phase of fact finding & analysis of the macro and micro ASEAN Healthcare environments.

The research focused on analysing the data available for the ASEAN countries in the healthcare space and from the experience and knowledge of the research partners working in these environments.

The analysis from the data was compiled into a preliminary report which is composed of the following sections:

- A section on the country sectors and their trends and direction, both over time and relative to each other.

- An ASEAN Economic Community progress assessment

- Initial identification of barriers and policy recommendations

Part 2 – Lifting-The-Barriers Roundtable

The Preliminary Paper was circulated to participants and attendees at the Network ASEAN Forum (NAF) Healthcare Roundtable to set the scene for discussion.

The Roundtable event was chaired by Dr. Lim Cheok Peng (IHH), co-chaired by Mr Kenneth Mays (Bumrungrad International Hospital) and moderated by Dr. Penny O’Hara (Accenture).

The format of the roundtable consisted of an introduction and personal overview of ASEAN healthcare from both Dr Lim and Mr Mays, followed by a brief précis from the Preliminary Paper.

The following discussion focused on those elements highlighted in the report and supplemented by observations and suggestions from the experience of Roundtable participants in the ASEAN healthcare landscape.

Suggestions, insights, observations and additional challenges were captured during the Roundtable discussion and highlights were given by Dr Lim and Mr Mays to the subsequent plenary session for inclusion into the final report.

Part 3 – LTB Report

The LTB Report has been completed through integrating the research conducted in Part 1 and the synthesised insights and observations from Part 2 in order to write the end deliverable as Part 3 – the Lifting-The-Barriers in ASEAN Healthcare Report.

NAF Healthcare LTB Roundtable list of attendees

The list of organisations participating at the Healthcare Lifting-The-Barriers Roundtable discussions

1. Accenture

2. Bumrungrad International Hospital

3. EAS Strategic Advice

4. Food Industry Asia

5. Halycon Capital

6. Heliconia Capital

7. IHH Healthcare

8. Johnson & Johnson

9. Khazanah

10. Malaysia Healthcare Travel Council

11. Medtronic

12. MuziHealth Consulting

13. Samsung

14. Sing Health

15. US Embassy- Commercial

Healthcare Lifting-The-Barriers Roundtable Observations – notes

Introduction from Dr Lim Cheok Peng – Healthcare LTB Roundtable Chair

Is the answer increasing the number of doctors?

“Historically, the majority of doctors functioned competently as generalists providing most of the care needs for patients, however with the advent of specialisations and even sub-specialisations, the ability to provide targeted and appropriate healthcare even in developed countries is facing difficulties. Where are these specialists? Are there enough?

How to address this shortfall? The private sector needs to help the governments train additional specialists in order to assist the public systems with fulfilling the numbers of doctors coming through specialised training. (From an IHH perspective, IHH runs a private university to train doctors enabling more advanced training).

So the healthcare players need to seriously consider training ourselves.”

Introduction from Kenneth Mays – Healthcare LTB Roundtable Co-Chair

“When we talk about the benefits of free trade and lowering barriers, we have to realise some important differences between healthcare and other sectors.

Liberalised trade allows countries to do what they are best at, and human resources and capital to flow more freely to where the competitive advantage lies. In ASEAN, this might imply a concentration of healthcare talent and resources in Thailand, Singapore and Malaysia, which provide some of the best healthcare quality and value in the world.

However, unlike electronics or automobile production, healthcare has both a commercial and public welfare side. The first priority has to be providing adequate care for the 98% of the population who gets their healthcare close to home. Only then can we realistically talk about lowering barriers for ASEAN citizens who cross borders for care, or for the millions outside of ASEAN who come to our famous medical centres for quality, service, and value they cannot find at home.

How do we promote our competitive advantages to medical travelers, while ensuring healthcare provision for local populations?

We need to be sensitive to the perception that medical tourism steals resources from local patients. In Thailand, medical tourists bring billions of dollars into the economy, both for medical services and spending on accommodations, food and shopping. However, the publicity of this success story has led to a concern among some that too much of the country’s medical resources are being diverted to care for foreigners. In reality, the numbers show that the country devotes less than 2% of its medical resources to realise the considerable benefits of being one of the world’s leading medical destinations. But the perception shows the unique feelings people have about healthcare.

The model for regional healthcare integration, therefore, needs to meet three criteria. First, it should encourage competition, innovation and value creation in the commercial sector. Second, it should lower barriers for the most capable medical centres to attract patients from both within and outside ASEAN. Finally, it should support the development of healthcare to acceptable quality and access levels in every ASEAN country.”

Roundtable Discussion topics

a. Manpower supply

- Which services require financing and delivery partners?

- Malaysia should not promote medical tourism until home country needs are fulfilled.

- Where ASEAN countries can help – more developed ASEAN countries, e.g. Singapore, Thailand, Malaysia, can support those in need through provision of expertise, training, guidance, policy, and planning, to move up the evolution chain

b. What does the ASEAN Healthcare landscape look like post 2015?

- How to leverage ASEAN integration?

- What is the impact of integration at national levels?

c. Increasing non communicable diseases (NCD) : impact on business community – how to improve working between sectors.

- E.g., food and beverage sector and healthcare.

- E.g., obesity and the lifestyle NCD – how do we deal with this?

- There is no regionalisation of that of the debate – it hasn’t been highlighted in ASEAN.

- Is there a policy gap question?

- Is there inadequate sharing gap question?

- How to bridge the gaps above? Is this through education or through control?

- Likely to be multifactorial – requiring multi sector /multi stakeholder input

- Put academic community together?

- Are these extremely knee-jerk reactions in how to solve the NCDs?

d. What is the speed to market of medications?

- There is income differentials and inequality in ASEAN affecting medications availability.

- Approval of new drugs can be a costly, lengthy process and have an adverse impact on patient outcomes

- Some countries don’t have the necessary means to be able to process new drugs rapidly.

- Monitoring and efficacy of medications is not consistent across ASEAN.

e. How to have infrastructure in place to ensure effective drugs reach the market more rapidly?

- E.g., steering committee to approve drugs in AEC for all the ASEAN countries

f. Medical guidelines are different between countries.

- E.g., consistency of health care provision – these may be influenced or impacted by the availability or otherwise of appropriate medicines.

- Make it easier to approve drugs. This is a good concept as currently each country has to prepare different documentation for effectively the same purpose.

g. High cost of healthcare and uneven distribution of available healthcare resources

- E.g., advanced care mostly available in towns and not in rural areas

- E.g., MRI scanners – can do only 10 scans per day – and not always fully utilised – in rural areas there are no MRI scanners, or in some cases under capacity in public institutions with waiting lists. Could there be slot sharing between institutions to maximise use?

- Improve Public/Private collaboration – opening up excess capacity from private provider to public hospital for training in medical school?

- Previously in Malaysia training of doctors in private sector was not allowed, can other countries follow suit and allow training of resources outside of public control?

- Need to distinguish specialised and common conditions, what can be treated where and by whom?

h. What do we mean by integrated healthcare across ASEAN?

i. Is ASEAN a “Melting pot” or “mixed salad”?

- Europe and the EU is more like a melting pot, similar cultures, unified currency, reciprocal basic health care provision.

j. It’s likely to be difficult reaching a melting pot in Asia – different currencies and culture – change is certain but right now – ASEAN is more like a mixed salad.

k. So what are the areas that can transcend geography and culture?

- What do patients want? Quality care, hotels to stay in , subsidies and insurance.

- Doctors – medical degrees – different governments need to acknowledge other country’s degrees – allow for freedom of movement for doctors, lifestyle and pay.

- Governments – Primary need is to take care of local population and secondary, allow overseas visitor or expatriate care.

- Universal drug approval process (EU has a process in place – Switzerland model)

- There is a movement in ASEAN to look at this and how to harmonise this.

Session wrap up and Plenary session

As part of the Healthcare Roundtable summation, Kenneth Mays identified a short list of initiatives. Priority should be given to the formation of a Pan-ASEAN drug approval process to improve delivery efficiency of drugs to markets across all ASEAN Member States (AMS). Cross border movement of medical personnel and medical training as well as visas for medical travel are equally important.

Dr. Lim stressed the importance of lobbying governments to change policy and speed up implementation. The increased participation of the private sector was key to achieving this. Several pressing issues also needed to be addressed in terms harmonisation of regulations, mutual recognition of skills and a common healthcare currency across ASEAN (e.g. France/UK cross border treatment) which could all be considered to accelerate integration. The development gap, a major integration barrier, could be overcome if better developed countries assisted less well developed countries in developing their talent and by outsourcing services to other AMS in the interim. These measures

underline the overall objective of good affordable healthcare to all in ASEAN.

Recommendation and NAF Feedback

- Most policy barriers can be addressed by acceding to commitments made or working with the respective committees formed by the AEC to harmonise regulatory gaps in the various healthcare sectors. Other legal barriers require dedicated efforts from the various governments to speed-up the passage of relevant laws and drafting of new regulations to facilitate the integration of healthcare across the region. However, the removal of explicit trade barriers may be insufficient for foreign service providers to enter the domestic market. Often, trade can only take off if countries are competitive enough and regulatory systems are made compatible.1

- Where ASEAN countries can additionally help – more developed ASEAN countries, e.g. Singapore, Thailand, Malaysia, can support those in need through provision of expertise, training, guidance, policy, and planning, to move up the evolution chain.

- Governments – The primary need is to take care of local populations. The secondary need is to allow overseas visitor or expatriate care where capacity allows is secondary.

Economic Barriers

Creating and providing a unified healthcare financing system across ASEAN countries at this present time is likely to be too challenging based on the extensive imbalance of member states’ progress, desire and capacity to deliver such an agenda. Early steps of providing some guidance to countries to evolve their local capability may be more constructive.

- Align the development of health financing schemes with structural shifts in the economy within each country’s own evolving health provision capability.

- Sustained economic growth is typically accompanied by increased urbanisation and a growing pool of formal sector as the economy shifts from an agricultural economy towards a service-based economy. Consider leveraging these shifts to increase health coverage by making participation to health financing schemes more attractive and subsequently target incremental increases in the coverage over time. This is particularly of high importance to less-developed economies where high out-of-pocket payments need to be reduced and government funds are limited. A study by the World Health Organization shows that all countries that have achieved the universal coverage have implemented necessary legislation to achieve compulsory participation.

- Improve the fiscal sustainability of healthcare funding through careful consideration of the costs and benefits of the design and structure of the financing schemes from an economic standpoint based on the starting points for each country.

- Validate the financial viability of social health insurance funds by carefully considering exemptions and exclusions. The inclusion of enterprises with high-paid workers will improve pooling between low-and high-paid earners, and also increase pressure on the funds towards improvement in the quality of benefits and transparency in management.2

- Gauge the costs and benefits of merging public and private health financing schemes for each country. For instance, shifting from free care for civil servants to social health insurance coverage will free up government resources, facilitate flexibility of movement between public and private sector employment and between salaried and self-employed status but may lead to higher out-of-pocket payments for healthcare for low-salaried civil servants.3

- Strengthen the ability to administer health funds by investing in the development of skills in the insurance administration and actuarial science at the level of the fund as well as in insurance regulation at the level of government

- Explore collaboration at the regional level to assist less-developed countries in establishing sustainable financing schemes for healthcare

- Identify possible investment opportunities for more-developed countries in establishing healthcare systems of less-developed countries.

- Share best practices for healthcare funding systems across ASEAN and leverage learnings to implementing social health insurance systems or other financing schemes, e.g. centralised provident funds, savings schemes, etc.

Labour Barriers

- Develop long-term human resource strategic plans at the national level to address labour shortages brought about by the regional integration

- Mobilise labour ministries in cooperation with health ministries to draw up a comprehensive plan that will address the country’s demand for healthcare professionals, factoring in external trends such as outbound migration, internal migration of healthcare workers due to entry of foreign health providers, and recent trends in medical education.

- Increase the supply of medical professionals through subsidies. Given that the private sector is also a beneficiary of medical graduates, it makes sense that they also share some of the cost to alleviate the burden from the government. This may be done through the private participation in medical training or tuition refunds for medical graduates from public universities moving to the private sector.

- Develop pay incentives, where labour shortage is severe. For instance, subsidise medical education of doctors in exchange for a fixed-term stay in rural areas to serve basic healthcare needs of the underprivileged or informal sector.4

- Accelerate training programs to build productivity and competitiveness of medical professionals

- Encourage foreign providers to bring in their specialists when establishing commercial presence in exchange of contributing their skills and knowledge to research programs or training programs in healthcare.

- Enter into partnerships with foreign health institutions to institutionalise cross-country training initiatives or exchange programs for medical professionals, internship programs or joint development of curriculums

- Leverage technology to develop a more skilled workforce. The availability of tele-education or training provided remotely over the Internet can help improve healthcare workers’ skills, allowing them to offer higher-quality, competitively priced healthcare services

- Allow for provision of the Private sector to help governments train additional specialists whom can assist the public system.

- Doctors – medical degrees – different governments need to acknowledge other country’s degrees – allow for freedom of movement for doctors.

Infrastructure Barriers

- Mobilise resources for upgrading infrastructure particularly in resource-strapped, less-developed countries in ASEAN by involving all available partners in the ecosystem, i.e. private sector, foreign donors and multilateral banks and financial markets

- Leverage technical assistance from external sources such as multilateral development banks and foreign official development assistance (ODAs) to finance critical infrastructure projects.

- Tap into the private sector as a source of private capital and expertise in developing sustainable infrastructure projects. In particular, public-private partnerships or PPPs represent an innovative way for the governments to work with the private sector in providing high-quality service delivery and in closing the gaps in fund requirements of the infrastructure sector.

- Improve Public/Private collaboration – opening up excess capacity from private provider to public sectors for resources and training in medical school.

- Access the banking market and capital market through bond issuance, bond rating and improved standing of public agencies as credible partners for the private sector.

- Build regulatory capacity in healthcare to support integration efforts

- Agree and establish a Pan ASEAN steering committee to approve drugs in AEC for all the ASEAN countries – expedite existing ASEAN harmonisation efforts.

- Strengthen regulatory systems by investing in capacity-building programs through increased collaboration with specialised international health agencies such as the World Health Organization and regulatory-focused organizations such as the Regulatory Affairs Professionals Society (RAPS) 5

- Augment human resource and expertise constraints by utilising available and competent frameworks from external sources. For instance, Singapore relies on the result of the product assessment and approval of certain ‘competent’ drug regulatory agencies (DRAs) in other countries for its own evaluation. This mechanism helps save time and resources needed for reviewing technical documentation on the part of the regulatory agency.6

Cultural Barriers

- Promote deeper intra-ASEAN social and cultural understanding

- Promote awareness about the AEC by engaging the public through educational campaigns and information dissemination on Southeast Asian studies and cultures. The inclusion of ASEAN cultures in national curriculums combined with exchange student programs to help foster greater understanding among ASEAN citizens. 7

- To help medical professionals appreciate and deepen their knowledge of ASEAN cultures, regional publications or dossiers can be produced to aid attending physicians in removing cultural and communication barriers in delivering care to foreign patients.

- Address concerns on the quality of care, accommodation, permissible subsidies and available insurances for patients seeking care overseas.

- Facilitate a change in mindset from a national towards a regional identity

- Develop a regional identity to be led by national governments who will commit to promote regionalism in the educational system, language, conflict resolution, etc. standardise English as a second language across the region to eliminate communication barriers in a region where multitude of dialects exist.

- Undertake activities that promote unity and solidarity across ASEAN members. Engage the mainstream media in promoting, on a continuing basis, all ASEAN programs and projects. Promote ASEAN sporting events in the national and private media such as the SEA Games and PARA Games. Encourage the use of ASEAN Anthem and other ASEAN Symbols to raise ASEAN awareness.8

- Explicitly establish open dialogues between industries that affect determinants of health, such as food and beverage and tobacco industries, and policy makers in healthcare.

Challenges identified

i. Barriers to integration

- At the highest level, outright non-trade policy barriers stand out as factors that impede healthcare integration in ASEAN. Most prominent are foreign ownership/equity limitations that inhibit the flow of capital into markets, restrictive laws or regulatory requirements that prohibit practice of the medical profession across the borders or restrict the movement of patients within ASEAN.

However, it is equally important to recognise that behind these policy barriers are interlinking core challenges that need to be addressed to achieve the objectives set by the AEC. Acceding to regional commitments and policy reforms to remove outright barriers are not sufficient to ensure that the region maximises the benefits of an integrated healthcare sector. For instance, the opening up of healthcare markets does not necessarily lead to increased foreign investments as demonstrated in Lao PDR, Myanmar or Cambodia. - Without accompanying developments in economic competitiveness, infrastructure, regulatory capacity or reforms in labour policies, access to healthcare remains limited.

There are four interlinking critical areas of development where several barriers exist that hampers the success of integration efforts in healthcare (see Figure 1).

- ASEAN has made progress in harmonising several regulatory gaps in healthcare. However, considerable effort is still needed. Outright policy barriers in healthcare still exist:

- Foreign equity restrictions. Only five out of the 10 member states have allowed full foreign ownership in their respective healthcare sectors. Malaysia, the Philippines, and Thailand only allow minority foreign ownership of 30%, 40% and 49%, respectively. Meanwhile, Indonesia’s Ministry of Health states a 90% foreign ownership limit in contradiction to the 100% limit in the investment policy. Myanmar has recently revised its foreign investment law and provides an 80% cap on foreign ownership for hospitals and clinics.

- Other legal barriers. In order to facilitate freer movement of foreign patients within ASEAN, certain laws need to be relaxed. Immigration laws and visa requirements across ASEAN do not provide preferential treatment for medical travellers. Visas are still required beyond the typical 30-day stay. Only Malaysia implements a “green lane” in its entry points and airports to facilitate easier travel for medical tourists. The absence of specific national laws also adds to the integration challenges. For instance, competition policy and law is integral to all four pillars of the AEC as it deals with various anticompetitive conducts, such as the abuse of monopoly power, cartels among businesses, merger and acquisitions which may affect market competition in a fully liberalised market. Of the 10 ASEAN Member States, only five have national competition laws (Thailand, Indonesia, Singapore, Vietnam and Malaysia).The rest are in various stages of drafting their own laws.

- Regulatory gaps. Gaps in various regulatory frameworks exist in healthcare. As discussed in the previous section, most of the ASEAN member states have yet to adopt and fully implement harmonised standards and MRAs that are critical to facilitating trade in health. For example, MRAs in medical professionals employed is hampered by the language requirement in regulations of some member states. Requirements by registration authorities of proficiencies in local language prohibit the recognition of relevant training even if standards of clinical care are similar. For example, medical professionals who want to practice in Thailand need to take the examinations in the local language.

- An equally if not greater challenge to healthcare integration are issues in areas of economic competitiveness, labour productivity and infrastructure including regulatory capacity development and cross-cultural integration. Meeting all policy and regulatory requirements may be accomplished on paper but preparations to prepare for the wider implications of a regional economy are lagging behind.

Economic Barriers

- One of the most urgent preparations needs to occur in the economic sphere. Currently, ASEAN member states are in different stages of economic development. Less-developed countries in ASEAN are burdened with fiscal challenges that limit resources allocated to support healthcare. Despite employing a mix of financing schemes, the coverage of healthcare in countries remains low and the population are forced to shoulder the costs of medical care (see Figure 2).

- In Myanmar, where there is no national health insurance, all public hospitals offer a medical cost-sharing plan – first introduced in 1993 – where patients cover the medicine and laboratory fees and the state pays the doctors’ fees.9 In Cambodia, health costs financing by households are mainly out of pocket payments. It is estimated that 80% of Cambodians use savings, go into debts or sell assets to pay for medical expenses.10 Both Cambodia and Myanmar have the highest private share in funding healthcare and high out-of-pocket expenditures despite having high poverty levels (see Figure 3). Thus, the economic burden of healthcare lies on the individual and contributes to even higher inequality and poverty.

- Even with liberalised markets, costs of healthcare in these countries will continue to be a burden given their low economic development. Poor economic climate directly impacts the affordability and availability of healthcare through inefficiencies and inadequacies in financing schemes. Entry of foreign providers is also unlikely to take place without significant economic reforms creating a viable healthcare market.

- Further, the perceived higher costs due to transportation and follow-up treatments and differences in the quality of care in foreign countries are major considerations that are likely to discourage these countries from taking advantage of cross-border healthcare services in the absence of financing schemes for healthcare.11

- Increasing economic competitiveness that can attract entry by foreign healthcare players entails improvements in labour and infrastructure. However, challenges exist in these areas as well.

- Provision of healthcare to medical tourists may divert medical resources away from the local population, however there are also benefits from medical tourism in that it brings additional money into the country and attracts top doctors back from overseas (the reverse of a brain drain). There needs to be a balance between the export benefits of medical tourism, and its resource costs. The tradeoffs need to be better explained to governments and the public, to avoid emotional reactions not based in fact.

Labour Barriers

- Labour shortage is one of the critical challenges of regional integration. Even middle-income countries such as Indonesia and Thailand are suffering from a shortage in healthcare professionals. In addition to losing manpower to outbound migration opportunities, less-developed countries are also likely to experience internal brain drain as markets open up to foreign players. Foreign providers are most likely to set up businesses in high-density urban areas and cities. This can draw out health professionals away from rural areas attracted by higher compensation and opportunities.

- On the aspect of mobility of healthcare professionals across ASEAN, discrepancies in standards and proficiency levels of personnel are crucial barriers. For less-developed countries, the lack of access to training facilities with sophisticated technologies and advanced knowledge of specialised treatments are limitations to the country’s ability to export health services and compete in the regional labour market.

- As technology and advancements in medical treatment become more complex and patient expectations rise, the need for medical specialists and even sub-specialists increases. However the shift in skillsets within the labour force is not matching the need and the ability to provide targeted and appropriate healthcare even in developed countries is facing a shortfall.

Infrastructure Barriers

- Some countries don’t have the necessary means to be able to process and approve new drugs rapidly and approval of new drugs can be a costly and lengthy process.

- High cost of healthcare and uneven distribution and coverage of existing healthcare resources in the country.

- Foreign direct investments in healthcare in less-developed countries will remain low despite full liberalisation if infrastructure remain underdeveloped and is not designed to handle the scale of global operations of providers. Both physical infrastructure such as well-developed network of roads, ports/airports; ICT infrastructure and supply chains and soft infrastructure such as digital penetration levels, regulatory capacity are requisites for critical factors that will determine the attractiveness of a country.

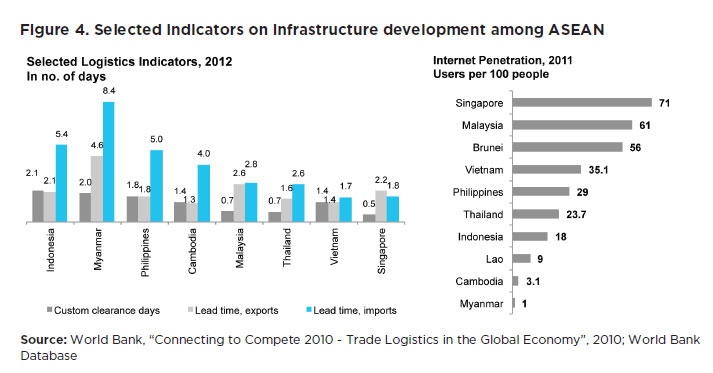

- There is a large imbalance in basic infrastructure existing among ASEAN member countries. For instance, only 14% of the total roads in Lao PDR are paved, compared to 57% in Indonesia and 80% in Malaysia.12 Indonesia and Myanmar have the longest lead time in imports, 5.4 and 8.4 days respectively, reducing its attractiveness as a hub for foreign players with global operations. The high trade and logistics costs in these countries lead to economic stagnation and discourage entry of foreign players in their markets (see Figure 4).

- Low digital connectivity and limited access to information and communication technology restricts technology transfer and the flow of information associated with delivery of health services.

- Weak regulatory capacity also presents an important challenge to integration. The lack of resources to dedicate for personnel re-training, up skilling and enforcement creates challenges in effective management of cross-border regulations. Individually, some member states also struggle to enhance their administrative capacity, either due to low budgetary allocations or cultural challenges. For instance, a major challenge among those with social insurance schemes is accelerating and expanding coverage. Efforts are frequently hampered by poor administrative capacity.13

Cultural Barriers

- The inter-relationship between determinants of health, such as diet, health and lifestyle and the incidence of Increasing non communicable diseases (NCD) such as diabetes, obesity, coronary heart disease and smoking related conditions has not been explicitly been made across ASEAN – how to improve working between sectors such as food and beverage industry, tobacco and health.

- Cross-cultural gaps and mindset are important factors slowing integration efforts. In labour, the difficulty of medical professionals to overcome language barriers, work around low health literacy among patients and embrace cultural practices in their host countries can impede effective delivery of cross-border health services. Conversely, patients’ lack of understanding and information on proper healthcare coupled with cultural beliefs in death, suffering and sickness has an impact on their treatment preferences and providers are barriers to accessibility of health services for foreign patients.

- The lack of a regional mindset among the ASEAN member states also feeds the low engagement levels by parties involved in the integration, ranging from patients, medical professionals, health providers and regulators. This partly stems from inadequate public awareness programs or information campaigns and mobilisation activities for which resources at the national level are limited.

Current State of AEC and areas of additional focus

i. The ASEAN Economic Community

- The ASEAN Economic Community (AEC) aims to achieve economic integration through four pillars:

- Single market and production base – Liberalise and facilitate free flow of goods, services, investment, skilled labour, and freer flow of capital

- Competitive economic region – Foster fair competition, protect consumer rights and intellectual property rights

- Equitable economic development – Accelerate the economic integration of less developed member states by technical and development cooperation

- Integration into global economy – Make ASEAN a more dynamic and stronger segment of the global supply chain

- One of the AEC’s key priority sectors is healthcare. The ASEAN Roadmap for Integration of the Healthcare Sector (Roadmap) covers five industries, four of which involve healthcare products: (1) pharmaceuticals, (2) cosmetics, (3) medical devices, (4) traditional medicines and health supplements.

ii. AEC’s Progress in Health Care

- Relatively more progress has been made in lowering trade barriers for healthcare in the region. Most of the region’s Common Effective Preferential Tariff (CEPT) rates were significantly lowered by 2003, and as of 2008, CEPT rates for most priority healthcare goods were at zero.14

- ASEAN has also identified non-trade barriers such as harmonisation of national standards with international standards, practices and guides; harmonisation of mandatory technical requirements to ensure free movement of goods; and harmonisation of conformity assessment procedures to save transaction time and to avoid high cost through multiple testing requirements as ways to respond to the challenge of addressing technical barriers to trade in ASEAN while at the same time ensuring that the aims of having systems of standards and conformance (which are to promote greater efficiency and enhance cost effectiveness in the production of intra-regional imports/exports) are realised.

- Collectively, developments are underway in completing regional initiatives that aim to establish an integrated ASEAN market in the identified healthcare goods – consisting of harmonised standards, registration and evaluation, an operable post-marketing surveillance mechanism, effective Mutual Recognition Agreements (MRA) – that would benefit consumers and economic growth:

- Relative to the three other healthcare goods sectors, there is better progress in harmonising standards for pharmaceuticals:

- MRA on Good Manufacturing Practice was signed by all the ASEAN countries in 2009, which provides for the sharing of inspection and registration information, represents another recent step forward in the cooperation effort.

The MRA became effective in 2011.15 - ASEAN Common Technical Dossier was also implemented in 2009, which gives information and format for the applications that will be submitted to ASEAN regulatory authorities for the registration of pharmaceuticals.16

- The MRA on the Post-Marketing Alert System (PMA) for pharmaceuticals has been set up and the system has been used initially by Brunei, Indonesia, Malaysia, Singapore and Thailand. The PMA is an efficient and effective system of alert on post-marketing issues affecting the safety and quality of pharmaceutical products.17

- The ASEAN Medical Device Directive (AMDD) — came out in 2012, and implementation is expected by December 2014. The AMDD lays out basic requirements for a harmonised classification system, medical device safety and performance, conformity assessments and a Common Submission Dossier Template (CSDT). The AMDD sets up a risk-based classification system of medical devices into four categories. Classification determines fees, processing times and clinical requirements. Currently, these issues vary among ASEAN countries. Individual countries may set up their own expedited registration channels under the AMDD framework, and they will have final authority over any classification disputes that may arise during the registration process. However, it is expected that many ASEAN member countries will follow the lead of Singapore, which has already implemented many of the AMDD directives.18

- The ASEAN Harmonised Cosmetic Regulatory Scheme, signed in 2003 is the flagship framework for regional cooperation in the field of standards and conformity assessment and in 2008, the ASEAN Cosmetics Directive came into effect.

- For the health supplement category, the output expected is the development of an ASEAN Regulatory Framework on Traditional Medicines and Health Supplements and transposition of the ASEAN Regulatory Framework into national laws of ASEAN Member States

- The healthcare services industry is the fifth segment of the healthcare priority sector. Healthcare services encompass a wide range of services and treatments provided by medical professionals and healthcare facilities such as hospitals, clinics, or laboratories. Trade in the ASEAN healthcare services industry is estimated to be smaller than trade in the four goods industries included in ASEAN’s healthcare priority sector. For example, in 2007, the world (including ASEAN countries) imported US$7.1 billion of priority goods from Singapore; in comparison, Singapore’s healthcare industry provided services to 348,000 patients, valued at S$1.7 billion (US$750 million). However, the designation of healthcare services in ASEAN’s healthcare priority sector reflects the industry’s increasing economic potential.

- The ASEAN Open Skies agreement initiated by the transport ministers in 2005 to accelerate the liberalisation of air travel has allowed regional budget airlines to enter the market and offer more flights between ASEAN destinations, such as Kuala Lumpur and Singapore or Kuala Lumpur and Yangon. The increased capacity in interregional air transportation facilitated intra-ASEAN travel of medical purpose.19

- According to the MOH Vietnam, around 40,000 Vietnamese citizens spend about VND 20.7 trillion (US$ 1.1 billion) on medical treatment services overseas each year. Vietnam can therefore be considered as a medical travel source market.20

- It is a common practice for Indonesians to seek HCS in foreign countries such as Singapore, Thailand and Malaysia for better quality healthcare. According to the Indonesian Medical Association, Indonesians spend more than 8.8 trillion Indonesian Rupiah (US$ 1.0 billion) per year on medical treatments overseas.21

iii. Unidirectional access to health migration

- To date, Thailand, Singapore, and Malaysia are the ASEAN region’s leading exporters of healthcare services. These three countries have developed a competitive advantage in healthcare with its ability to offer the same medical services at significantly lower price relative to developed countries and a reputation for high quality services. Thus, they are well-positioned to become healthcare hubs of the region, given the expected strong growth in medical tourism.

- Singapore, Malaysia, Brunei and Thailand are beneficiaries of migration patterns and are net labour recipients, i.e. they have greater stock of labour from ASEAN than they send to the rest of ASEAN.

- With respect to an integrated health market, increased mobility of healthcare professionals may exacerbate the shortage in medical talent in other parts of ASEAN, although certification or language requirements in certain countries are an existing barrier to healthcare professional entry. The region as a whole also faces stiffer competition for healthcare professionals. Countries such as Singapore and Malaysia become transit countries for those foreign nurses seeking further migration. Estimates place the shortage of physicians in ASEAN at 1.6 million, the highest among regions in the world.22

- ASEAN is a very diverse region. It is composed of a group of countries with unique political, cultural, economic and social characteristics.

- From the perspective of healthcare, we see that member countries are at varying levels of development due mainly to significant differences in resources spent on health, access to healthcare, and healthcare supplies such as pharmaceuticals.

- Higher-income countries like Singapore, Malaysia and Thailand have healthier populations due to higher expenditures on healthcare while Lao People’s Democratic Republic (PDR), Cambodia and Myanmar are grouped at the other end of the spectrum with higher mortality rates and lower per capita health spending (see Figure 5).

i. The haves vs. the have-nots

- Not surprisingly, higher-income countries are well-ahead of the lower-income ones in terms of resource availability for health, healthcare coverage and quality of care (see Figure 6).

- Singapore, Brunei and Malaysia, with their low population bases enjoy a surplus in healthcare resources with higher-than-average availability of medical personnel and facilities.

- Lao PDR, Cambodia and Myanmar suffer from severe resource deficits to respond to the healthcare needs of its citizens. For every 1,000 of its population, less than 1 doctor and nurse is available and less than 10 hospital beds for every 10,000 people is available.

- Middle-income economies such as Philippines, Vietnam and Indonesia have barely adequate healthcare resources to cover the health needs of its large population. Indonesia, for example, with more than 240 million people sees a deficit in doctors and hospital beds. Vietnam, with 89 million people, has less than 1 nurse for every 1,000 people.

- Singapore, Malaysia, and Thailand have been able to leverage on the surplus of some of their resource bases to expand the coverage and develop the quality of their healthcare capabilities. These countries stand out as healthcare centres with results comparable with that of the US or UK. For instance, the number of births attended by skilled health personnel and immunisation coverage of children for measles in these countries is equal if not higher than in the US and UK. Neonatal mortality rates for them are the lowest and case-detection rates for tuberculosis are the highest in the ASEAN region.

- In contrast, Lao PDR, Cambodia and Myanmar have the highest mortality rates at childbirth and poorest detection rates for tuberculosis in the region, indicating the shortfall in quality and coverage of healthcare services.

ii. The evolving healthcare landscape in the region

- Increasing affluence. As the level of income rises with economic development, the landscape for healthcare will evolve. At the broadest level, continued economic growth will cause a transition into more discretionary areas of healthcare spending. Between 2000 and 2010, healthcare spending by Southeast Asia’s middle class grew over 9% annual compound rate. The Economist estimates that healthcare spending in Asia has risen from 14% of the global total in 2006 to 23% in 201223. As some ASEAN populations become wealthier and more people join the middle class population, the region will witness more discretionary areas of healthcare spending although the gap between the haves and have-nots may grow wider.

- Increasing aging population base. Demographic shifts on population age structures will increase the burden of healthcare costs even for developed countries in ASEAN. Across the region, a demographic transition is set to occur in the coming decades where the population of older than 65 years old will double and comprise 10% of the population. Together with longer life expectancy, the dependency ratio across ASEAN will jump to 23% by 2050 from 10% in 2015 and increase the burden of healthcare costs. This demographic shift will be more pronounced for well-developed nations with higher ageing populations and longer life expectancy rates (see Figure 7)

An ageing population leads to an increase in the demand for healthcare due to higher occurrence of non-communicable lifestyle diseases such as cardiovascular diseases as well as cancer and age related diseases such as arthritis and diabetes, among others; higher requirement for diagnosis and hospital-based inpatient and outpatient treatment; and longer duration of care.

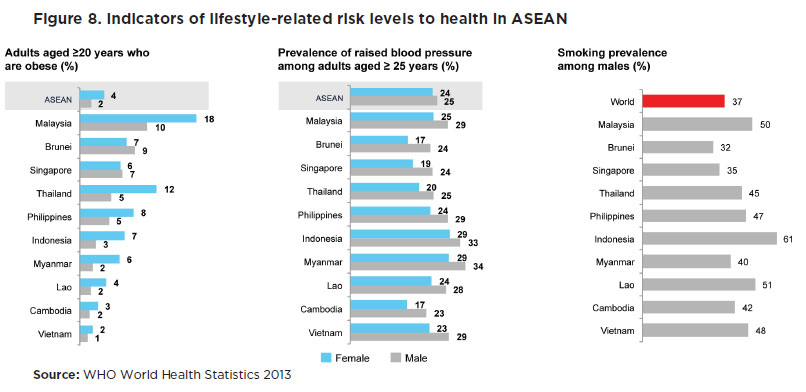

An ageing population leads to an increase in the demand for healthcare due to higher occurrence of non-communicable lifestyle diseases such as cardiovascular diseases as well as cancer and age related diseases such as arthritis and diabetes, among others; higher requirement for diagnosis and hospital-based inpatient and outpatient treatment; and longer duration of care. - Elevated health risk of ASEAN populations. Relatively higher population growth rates and increased urbanisation in the ASEAN region will increase overall health risk. Southeast Asia will add more than 131 million people in its cities, increasing the risk of communicable diseases from high-density urban life brought about by higher population density and poor living conditions. Along with urbanisation comes socio-cultural developments that are detrimental to health conditions. Today, non-communicable diseases (NCDs) are top killers in ASEAN causing 7.9 million deaths annually. This is expected to increase by 21% over the next decade24. Much of NCDs are caused by lifestyle-related factors leading to hypertension, obesity, and respiratory diseases (see Figure 8).

iii. Can ASEAN respond to the call of increased healthcare demand?

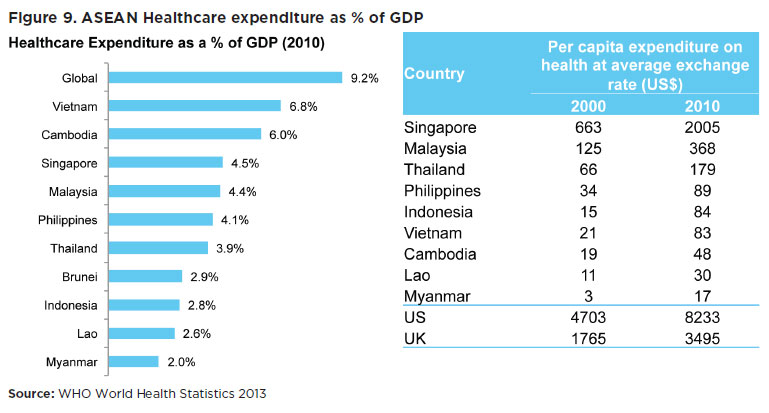

- Funding for healthcare. Meanwhile, the majority of ASEAN countries struggle to respond to the increasing healthcare demands due to their limited resources. Across ASEAN, healthcare spending remains low. The global average for health expenditure is at 9.2% of GDP. ASEAN countries spend less than global peers. On a per capita basis, Singapore spends the highest on healthcare, more than six times the amount that Malaysia spends and more than a hundred times that of Myanmar’s health expenditure per capita (see Figure 9).

- Most countries in ASEAN employ a mix of healthcare financing schemes. Several have socialised health insurance schemes covering certain segments of the population, such as employees of public departments, workers from formal and informal sectors and their families, mostly covering sectors where premiums or contributions could be collected easily. There are efforts underway to expand the social health insurance schemes to achieve universal or near-universal coverage in some countries by combining social health insurance and direct subsidies or community-based financing coming from public revenue/funds but few have been successful so far.25

- Countries such as Thailand, Vietnam, Philippines and Indonesia have employed risk-pooling through social health insurance schemes. However, coverage remains low and thus still needs to be complemented with government revenues to become universal. Also, most schemes also cover mainly financial risk for hospital care and exclude other significant costs of health care such as transportation, medicines, follow-up consultations, etc.

- Lao PDR and Cambodia, both resource-poor countries, have mostly relied on donor-supported health equity funds to reach the poor, and reliable funding and appropriate identification of those eligible are two major challenges for nationwide expansion.

- Malaysia and Singapore both use a mix of financing schemes involving compulsory saving schemes and provident funds.26

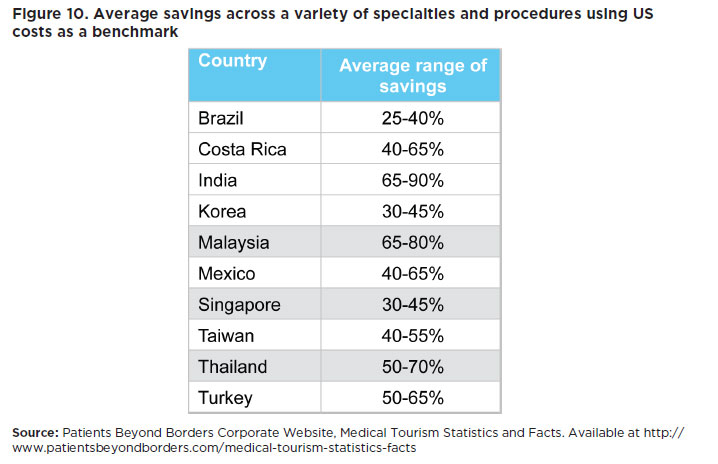

- Funding aside, migratory patterns driven by a mix of push and pull factors are enabling access to, and the delivery of healthcare services in some countries much easier and more economical. In general, higher wages and better employment opportunities enable Singapore, Malaysia and Thailand to attract medical professionals and healthcare workers. Hence, high-income countries are already the preferred destination for quality healthcare by foreign patients due to the cost savings these countries can offer (see Figure 10).

iv. Member state initiatives to improve national health

- Individually, the member states have made progress in a number of specific areas to improve their healthcare industries in their respective jurisdictions.

- SingaporeMedicine, an initiative between Singapore Tourism Board, Ministry of Health and Economic Development Board and IE Singapore is a collaborative effort to promote the Singapore brand overseas. Launched in 2003, SingaporeMedicine is committed to strengthening Singapore’s position as Asia’s leading medical hub, and promoting Singapore as a world-class destination for advanced patient care.

- In Malaysia, the Malaysia Healthcare Travel Council (MHTC), a government agency under the Ministry of Health Malaysia has been set up to develop and promote the healthcare travel industry and to position Malaysia as the healthcare destination of choice in the region. MHTC is a focal point or a ‘one-stop centre’ for all matters related to healthcare travel, to facilitate enquiries on policies and programmes on healthcare travel development and promotion, and serve as a one-stop centre for solutions on matters related to healthcare travel. They are also the referral point to assist healthcare travellers and members in the healthcare travel industry in Malaysia

- Brunei has been stepping up efforts to leverage cross-country trainings through bilateral agreements. Brunei signed a series of memorandums of understanding (MOUs) on healthcare training and healthcare services with Singapore in the last 9 years and a MOU on healthcare services with Thailand in 2010. Thirteen doctors from Brunei have completed courses in various clinical expertise fields between 2010 and 2013.27

- Indonesia has laid down the framework towards providing universal health coverage for its population. The central government is preparing for the implementation of universal health coverage for all as mandated in the Social Security Providers (BPJS) Law and expects to have the law’s executing body established and operational by January 2014. The commitment for universal health coverage is set by 2019.28

- There is a move towards universal health coverage in the Philippines as well with the amendment of the national health insurance law providing that all citizens of the Philippines, regardless of social and economic status, shall be covered by the national health insurance protection. However, enrolment in the NHIP shall not be made compulsory in certain provinces and cities until such a time that the Philippine Health Insurance Corporation shall be able to ensure that members in such localities shall have reasonable access to adequate and acceptable health care services.29

Endnotes

- World Bank, “Trade in Health Services in the Asean Region, 2007

- World Health Organization, “Social Health Insurance: Selected Case Studies from Asia and the Pacific, 2005

- Ibid

- World Bank, “Trade in Health Services in the Asean Region, 2007

- Regulatory Focus, Asian Regulatory Harmonization Plan Calls for Investments in Regulatory Capacity, October 25, 2012, http://www.raps.org/focus-online/news/news-article-view/article/2463/asian-regulatory-harmonization-plan-calls-for-investments-in-regulatory-capacity.aspx

- S. Ratanawijitasin, “Drug Regulation and Incentives for Innovation: The case of Asean”,

- Institute of Southeast Asian Studies, “Towards Realizing an Asean Community: A Brief Report on the Asean Community Roundtable,

- Association of Southeast Asian Nation, “Roadmap for an Asean Community 2009-2015”

- IRIN Asia, “MYANMAR: Call for new government to boost health spending”, April 4, 2011 http://www.irinnews.org/report/92352/myanmar-call-for-new-government-to-boost-health-spending

- International Labor Organization, “SOCIAL SECURITY EXTENSION INITATIVES IN EAST ASIA”, Date http://www.ilo.org/public/english/region/asro/bangkok/events/sis/download/paper29.pdf

- World Bank, “Trade in Health Services in the Asean Region, 2007

- World Bank Database

- World Health Organization, “Regional Overview of Social Health Insurance in South-East Asia”, July 2004

- United States International Trade Commission, “ASEAN: Regional Trends in Economic Integration, Export Competitiveness, and Inbound Investment for Selected Industries”, August 2010

- International Pharmaceutical Quality, “ASEAN Effort Progressing on CMC/GMP Harmonization, But Differences Remain”, December 20, 2010

- Ibid.

- National Pharmaceutical Control Bureau, Malaysia, and Health Sciences Authority, Singapore, “ASEAN Post-Marketing Alert (PMA) System – The Malaysian and Singapore Experience, July 20, 2007

- Pacific Bridge Medical, “Medical Device Harmonization in Southeast Asia’, July 18, 2013

- United States International Trade Commission, “ASEAN: Regional Trends in Economic Integration, Export Competitiveness, and Inbound Investment for Selected Industries”, August 2010

- Frost and Sullivan, “Independent Market Research on the Global Healthcare Services (HCS) Industry, June 1, 2012

- Ibid

- World Health Organization, “Working Together for Health: World Health Report 2006”

- Pacific Bridge Medical Website, “Asia’s Rising Middle-Class to Drive 10-Year Healthcare Growth”, March 1, 2012

- World Health Organization, Noncommunicable diseases in the Southeast Asian Region, 2011

- World Health Organization, “Regional Overview of Social Health Insurance in South-East Asia”, July 2004

- World Health Organization, “Social Health Insurance: Selected Case Studies from Asia and the Pacific, 2005

- The Brunei Times, “Brunei, S’pore fortify efforts in health and medicine”, May 29, 2013

- A. Simmonds, K. Hort, “Institutional analysis of Indonesia’s Universal Health Coverage policy”, May 2013

- GMA News Online, “New law provides PhilHealth coverage to all”, June 21, 2013

![]()

RELATED REPORTS

- ASEAN SHOULD FOCUS ON HEALTH TOURISM, ASEAN-WIDE HEALTH INSURANCE, AND TALENT MOBILITY

- LIFTING THE BARRIERS REPORT FOR ASEAN HEALTHCARE

- LIFTING-THE-BARRIERS REPORT 2015: HEALTHCARE