How COVID-19 will transform global supply chains and how ASEAN must respond

KEY HIGHLIGHTS

-

- The rapid spread of COVID-19 has impacted manufacturing the world over. ASEAN industries in particular are in for a painful 2020 due to supply chain disruptions centering on China.

-

- The modern nature of supply chains, with their focus on lean manufacturing and supplier consolidation, has put them at greater risk of disruptions.

-

- According to IHS Markit PMI data, ASEAN manufacturers saw their worst month on record in March 2020, due in part to supply chain disruptions impacting factory production and delivery times.

-

- There are several scenarios for how the COVID-19 pandemic could play out and its economic ramifications, including a seasonal disruption, prolonged disruption, an uneven rebound, and a global rebound.

-

- Multinationals looking to hedge against future supply chain disruptions may look towards diversifying their production bases away from China, or reshoring production back home.

- ASEAN should respond to these expected shifts in global trade by advocating for greater intra-ASEAN trade and investment, pushing ASEAN towards becoming a single market to increase its competitiveness, recognising public health as a new dimension of global trade, and guarding against any rise in global protectionism by defending the rules-based international order.

A disruption in supply and demand

As of April 10, 2020, there have been over 1.6 million confirmed cases of the respiratory virus COVID-19 worldwide, along with over 95,000 deaths. The virus has had an unprecedented impact on world economic activity, with many major global economic and financial centres, including New York City, London, Tokyo, Hong Kong and Singapore, under some form of a lockdown or undergoing significant restrictions in mass gatherings and business operations. Travel restrictions have been imposed by over 150 countries, accounting for the vast majority of travel demand.1

After a shutdown and now gradual recovery of Factory Asia, we are now seeing a shutdown of Factory Europe and America, with the impact of the coronavirus outbreak having shifted from the services sector to manufacturing. This has caused shutdowns in heavy industry in the West not seen since the Second World War.2

ASEAN manufacturing: the China Factor

2020 promises to be a painful year for ASEAN’s export-orientated economies – many of whom serve as key supply nodes within the intricate regional production networks centring on China. ASEAN serves as a major supplier of intermediate goods and commodities to China, who process them into finished goods for export to the West.

Likewise, much of ASEAN’s own domestic manufacture, from electronics to textiles, depend on Chinese-made components and raw materials. The rapid spread of the coronavirus, and the subsequent lockdowns governments imposed to contain it, thus saw disruptions in global value chains through both demand and supply.

The vulnerabilities of modern supply chains

Beyond an over-dependence on China, pundits have pointed to the unique vulnerabilities of modern global supply chains which have been laid bare by the COVID-19 pandemic. Recent attempts by global businesses to reduce supply chain costs through a focus on lean manufacturing, offshoring, and supplier consolidation by concentrating manufacturing while also reducing inventory levels that limit businesses’ reactive capacity in case of disruptions has paradoxically increased overall global supply chain risk. . Supply chains have ultimately become more integrated, but at the same time less flexible.

This was evidently seen in how many businesses were seemingly caught off guard by the pandemic. 71% of businesses surveyed by The Economist in February would state they had no business operations contingency plan in case the outbreak lasted longer than a few weeks.3

Freefall of China’s manufacturing sector

The initial outbreak of the coronavirus in Wuhan would have a severe impact on Chinese manufacturing. According to numbers by China’s own National Bureau of Statistics:

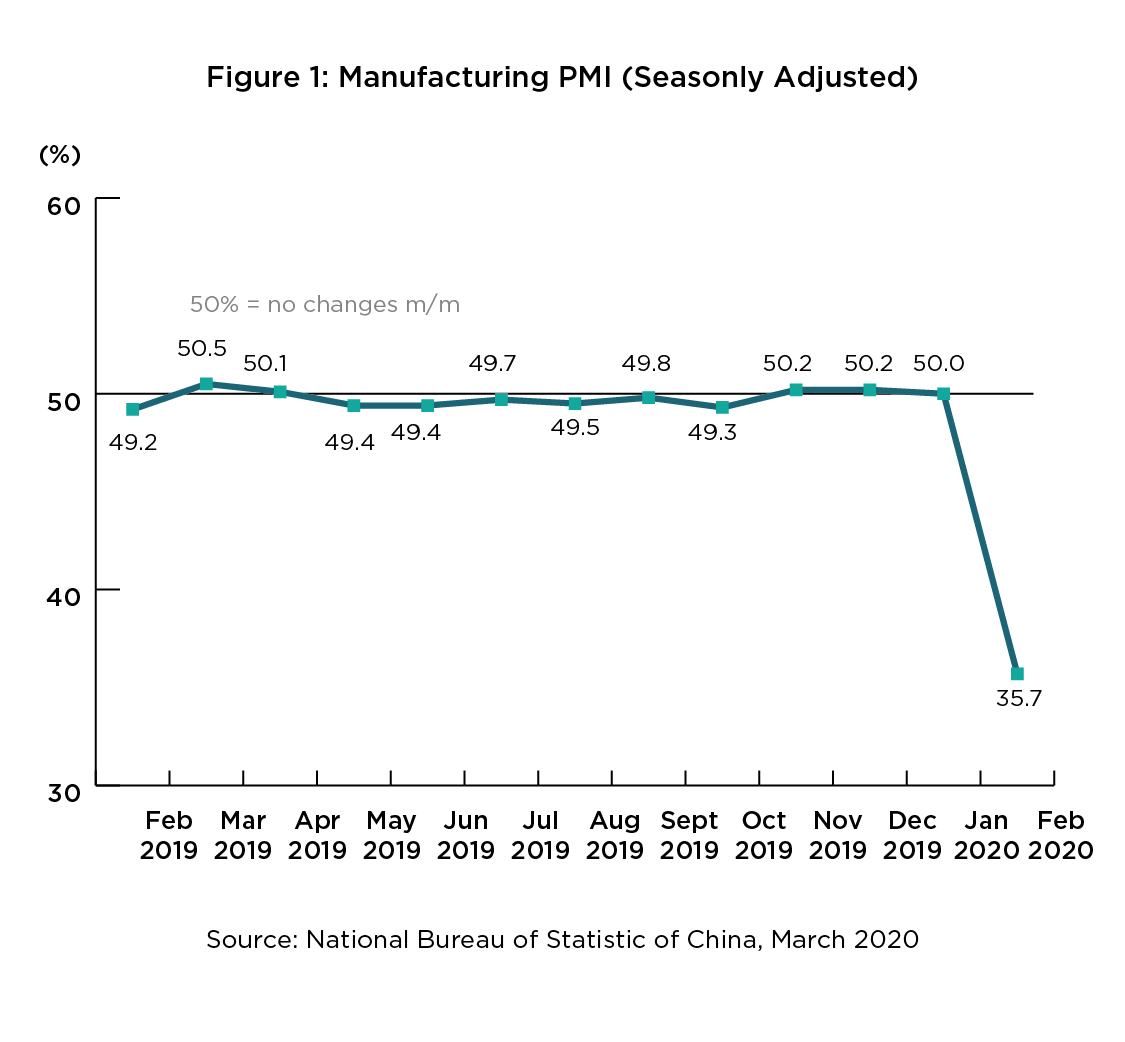

- The Manufacturing Purchasing Managers Index (PMI), a measure of factory activity across the country, plummeted to a record low of 35.7 in February 2020, down from 50.0 the month before (see Figure 1).4

- The production index in February 2020 was 27.8%, dropping by 23.5% from the month prior, indicating a slowdown in manufacturing production activity.5

Supply chains in ASEAN severely disrupted

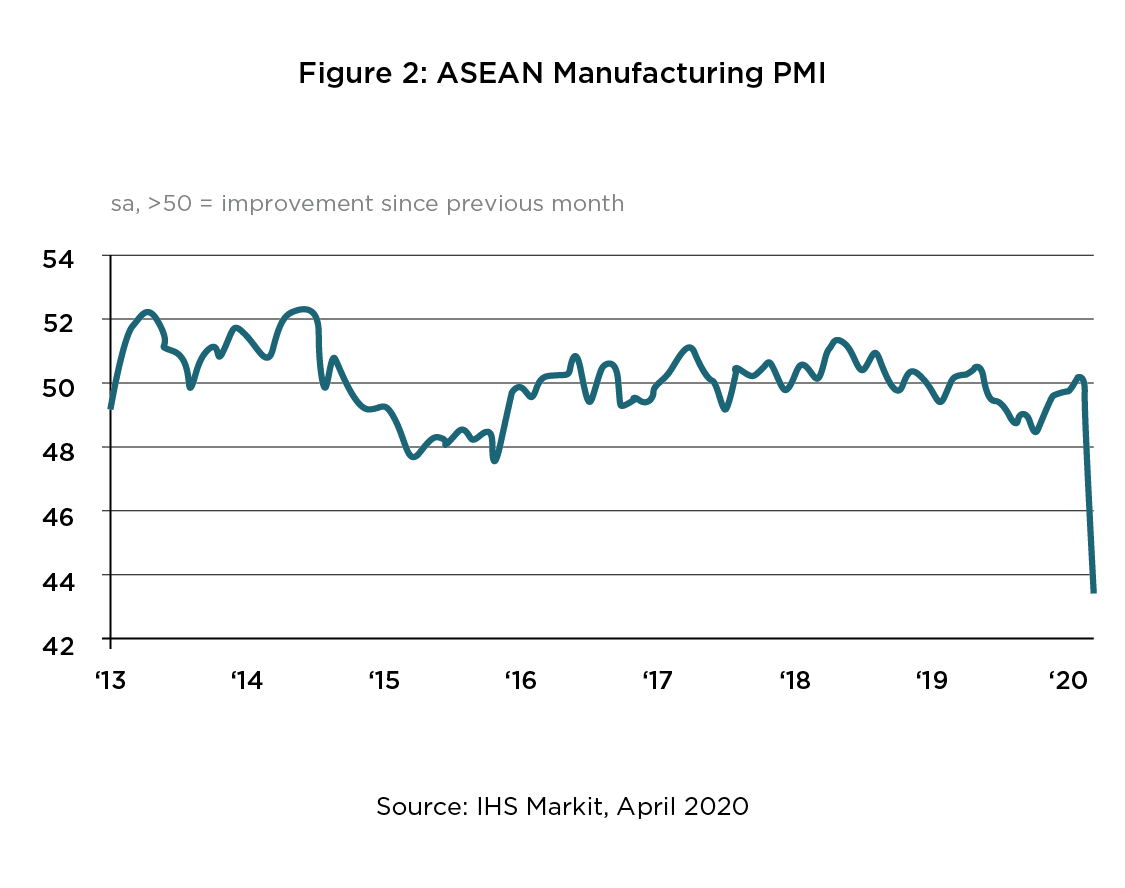

Like the virus itself, the economic impact has spread quickly to Southeast Asia through the disruption of the supply of raw materials, labor, and sub-assembly components. According to IHS Markit’s PMI data, ASEAN manufacturers saw their worst month on record in March 2020, with the headline PMI falling from 50.2 in February to a record low of 43.4 in March (see Figure 2). 6

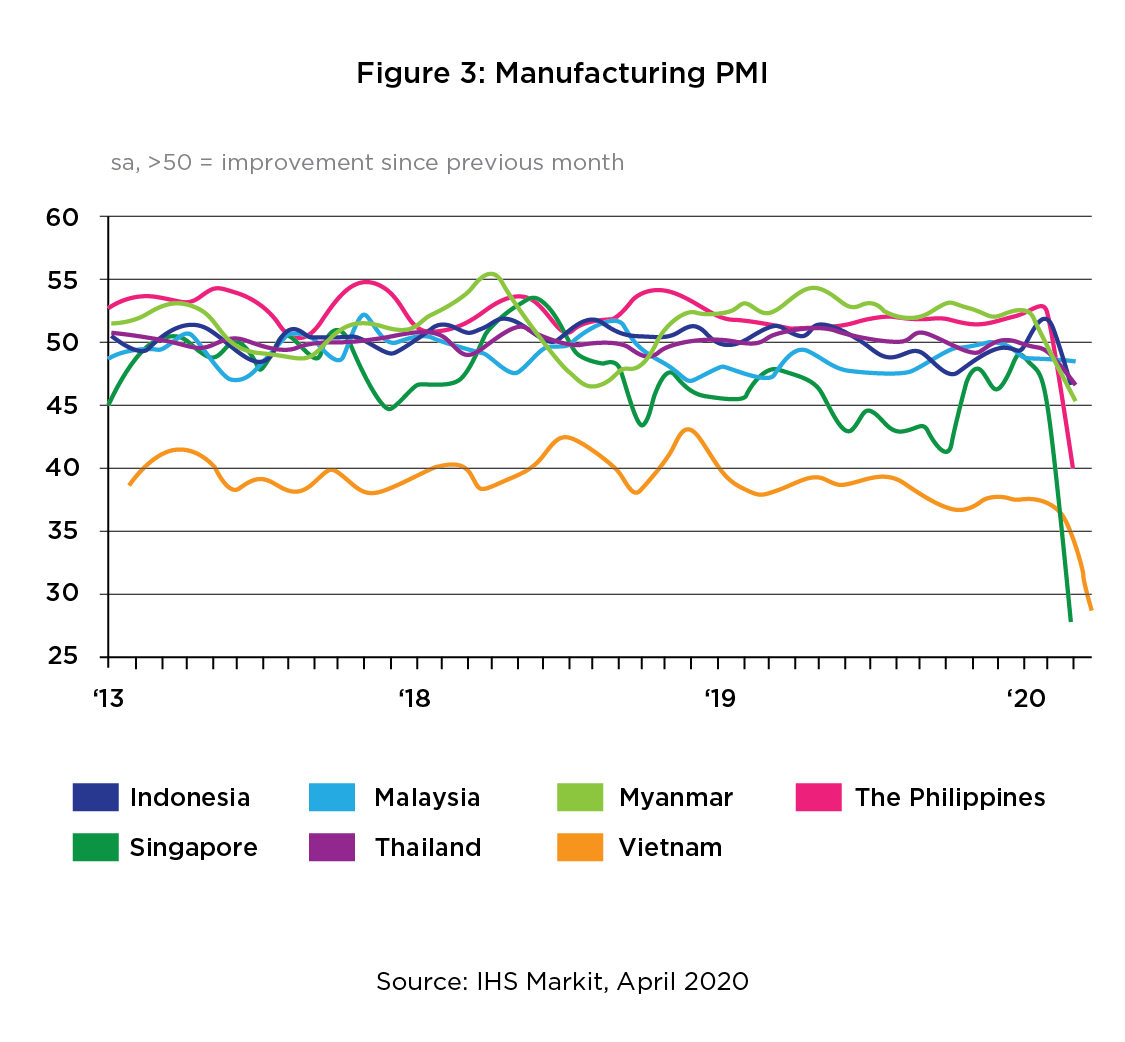

Deteriorations were reported in each of the seven constituent economies that IHS Markit covered. The downturn was most marked in Singapore, with the headline figure in March slipping a record 18.1 points month-on-month to 27.7, its lowest score in the eight-year history of the survey (see Figure 3).7

The drop was attributed to deteriorating operating conditions for manufacturing firms, with record declines in production output and new orders in particular driving the downturn. Disruptions in supply chains impacted factory production and caused delays in delivery times.8

ASEAN industries in trouble

Numerous industries across ASEAN, several of whom are major domestic employers within their respective economies, would report being impacted by supply chains disruptions linked to China. These included:

-

- Tech firms in Malaysia’s state of Penang, one of the world’s largest electronics and electrical hubs, warning of disruptions in supplies from China and therefore to their revenue growth outlook. Many of these firms supply major tech multinationals such as Intel, Apple, and Broadcom, and rely on China for as much as 60% of components and materials.9

-

- Textile firms in Cambodia and Vietnam faced disruptions in the supply of raw materials from China. Cambodia’s garment industry employs some one million full-time workers, and procures some 60% of its textiles from China.10

- Factories in Indonesia have complained of supply disruptions of raw materials, with an estimated 20% to 50% of the raw materials for the country’s factories being sourced from China alone. The government was forced to step in to provide relief measures such as six-month relief from income tax for workers in the manufacturing sector and delays in import and corporate taxes for businesses.11

According to a February 2020 survey by the American Chamber of Commerce in Singapore, a majority of firms in the logistics, manufacturing, and technology sectors stated that the pandemic had impacted their business operations (see Figure 4).

Given Singapore’s position as a regional hub for the larger Asia-Pacific region for many multinationals, the impact on firms in the country is possibly indicative of larger disruptions to regional supply chains.

Supply chain disruptions have not only impacted manufacturers but also those in the services sector. A survey of 150 finance executives from around the world by PricewaterHouse Cooper (PwC) during the week of March 23 concerning the pandemic saw 36% responding that they were considering making adjustments to their supply chains (see Figure 5).

How bad can it get?

Global risk intelligence consultancy Control Risks lays out four scenarios for the COVID-19 global pandemic, with focus on the implications for global supply chains (Table 1).12

Future implications for global supply chains

In the long term, global businesses hoping to hedge themselves from future supply chain disruptions can respond through two main strategies:

-

- Supply chain diversification: the global pandemic has revealed the inherent risk of firms directing all of their demand for intermediate goods and raw materials to a single source. Companies in the future may decide to diversify their production bases to hedge against future supply shocks, regardless of the immediate cost benefits.

We may see a greater relocation of production from China to Southeast Asia in light of the pandemic, but as Thai Ambassador to Malaysia H.E. Narong Sasitorn noted in a recent CARI ASEAN Roundtable Series, ASEAN would first have to demonstrate they collectively understand the opportunities being provided to them in order to attract investors.13

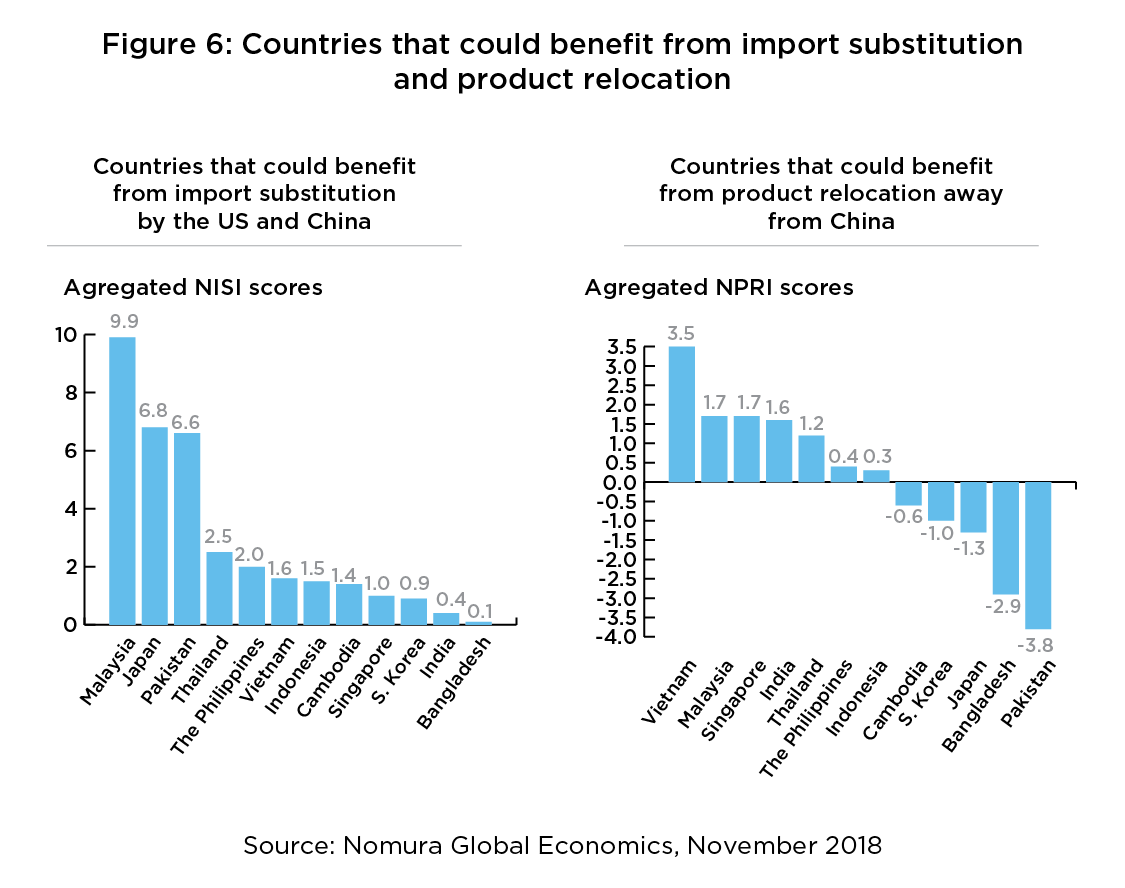

A 2018 study by Nomura identified Malaysia, followed by Thailand and the Philippines, as the biggest potential beneficiaries among select Asian countries of import substitution by US and Chinese firms during the US-China Trade War (see Figure 6).14

The study similarly identified Vietnam, followed by Malaysia and Singapore, as the most likely Asian countries in diverting production and FDI away from China during the same period (see Figure 6).15

Both of these findings may be replicated by companies seeking to diversify their sources of production in the wake of the COVID-19 pandemic, assuming ASEAN leaders can correctly identify the opportunities and take advantage of them.

*Nomura utilized the Nomura Import Substitution Index (NISI) to identify which Asian countries would benefit the most from Chinese and US import substitutions (e.g. importing from other countries due to tariffs imposed).

**They also used the Nomura Production Relocation Index (NPRI) to identify which countries would be most successful in diverting production and FDI from China.

- Onshoring of production: the exposure of the inherent fragility of modern supply chains may persuade some companies to produce more of their goods locally. The advent of the Fourth Industrial Revolution (4IR) and the increasing automation of manufacturing has made it more economical to shift production back to developed economies where the costs of labor is less material. This has been referred to as onshoring or near-shoring.

SHEA Global, an automation technologies consultant, noted that such as artificial intelligence (AI) and augmented reality (AR) will allow future workers in the manufacturing sector to work remotely and thus to continue operations during disruptions, mitigating future workplace health risks in the process.16

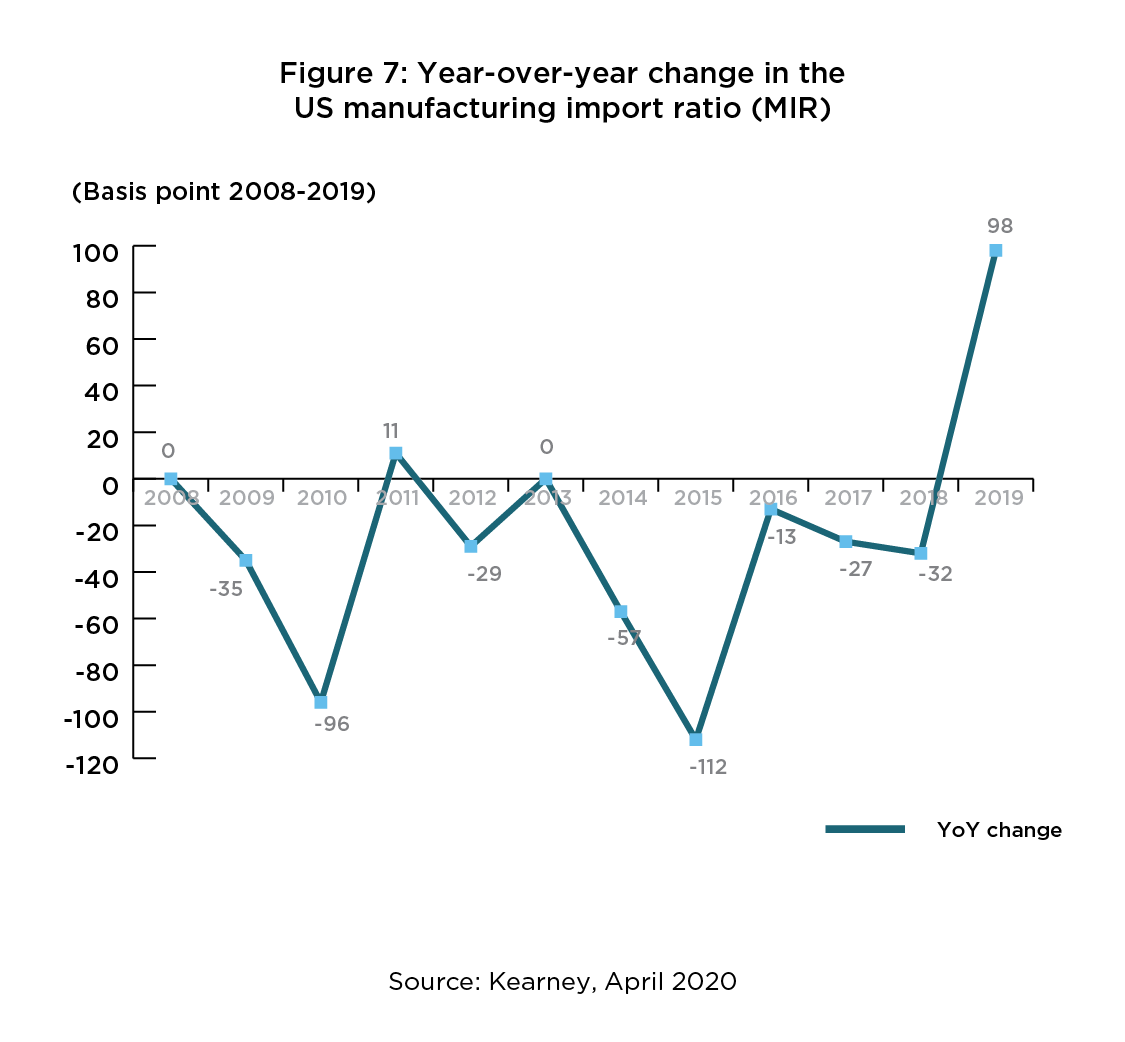

The seventh annual Kearney US Reshoring Index, which compares US manufacturing gross output to the import of manufactured goods from 14 Asian low-cost countries* (LCCs) proves illuminating. The US Reshoring Index is expressed in basis points (1 percent change = 100 basis points). A positive index number indicates net reshoring – the degree by which gross domestic output exceeded imports from the 14 LCCs as compared to the previous year. 17

The resulting 98-basis point jump in the Kearney Reshoring Index in 2019 is by far the highest yet registered by the index (see figure 7). Kearney attributed this almost exclusively to a collapse in imports from China, which declined by 17% in value terms due to US tariffs. By a substantially increased margin, US companies chose to source more goods domestically rather than import them from the Asian LCC countries. 18

Kearney argued that COVID-19 will further force companies to rethink their sourcing strategies by factoring in resilience (the ability to foresee and adapt to unforeseen systemic shocks) as a new dimension of global supply chains.19

- Supply chain diversification: the global pandemic has revealed the inherent risk of firms directing all of their demand for intermediate goods and raw materials to a single source. Companies in the future may decide to diversify their production bases to hedge against future supply shocks, regardless of the immediate cost benefits.

The path forward for ASEAN

Given the disruptions and projected long-term changes to global supply chains, there are different ways ASEAN can respond:

-

-

- Push for greater intra-ASEAN trade and investments: in light of ongoing fracturings of global supply chains and shifts towards onshoring of manufacturing, ASEAN should seek to hedge themselves in the long term by pushing for greater intra-regional trade and investment. Greater regional connectivity can help strengthen the bloc in an increasingly uncertain trading environment and make the region less dependent on external markets such as China.

-

-

-

- Building a competitive ASEAN single market: for multinationals who seek to diversify their future production bases (instead of producing their goods locally) , many will no doubt turn to Southeast Asia for alternative manufacturing sites. ASEAN must be cognizant of these trends and expedite liberalisation reforms and push ASEAN towards a single market in order to better compete with larger markets such as China and India.

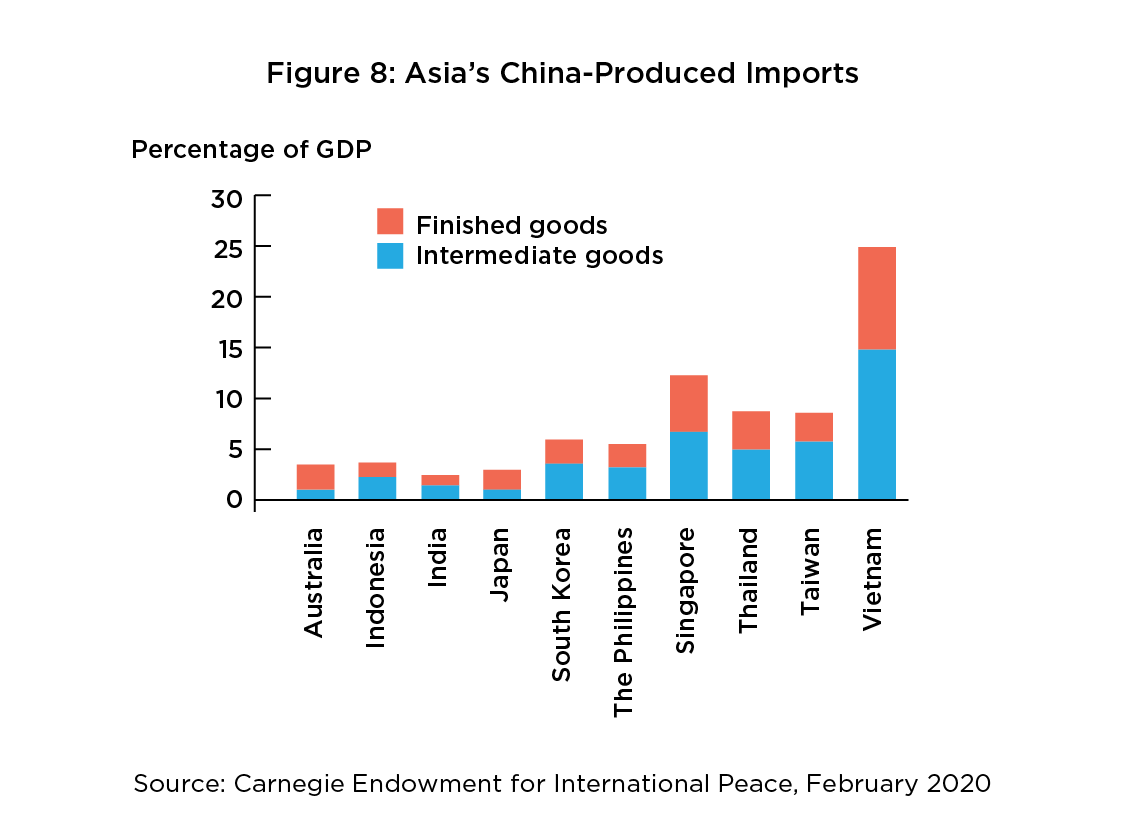

However, caution must be practised. Even if ASEAN firms were to benefit from import-substitution and production relocation vis-a-vis China, the complexity of modern supply chains means these firms may themselves may be dependent on Chinese supplies of raw materials and sub-assembly components. To put this into better perspective, data from the Carnegie Institute revealed that countries like Vietnam, Philippines, and Indonesia imported a larger proportion of Chinese-made intermediate goods than finished goods (see Figure 8). Most multinational corporations (MNCs) today are often unaware of the full extent of their supply chains below their top tier (direct) suppliers. 20

There are often no direct contractual relationships between MNCs and their lower tier suppliers. This leads to increased risk and challenges in managing the lower tier suppliers as they are further removed from the MNC’s direct supervision. It will be prudent for firms moving forward to exhaustively map out their supply chains to help determine the full extent of their vulnerabilities to future disruptions. 21

- Public health as a new dimension of global trade: in relation to the previous point, the COVID-19 pandemic has added a biological dimension to the political and institutional challenges of contemporary global trade. Future investors may be wary of investing in or trading with countries with inadequate public health infrastructure that would struggle to handle pandemics such as the coronavirus.

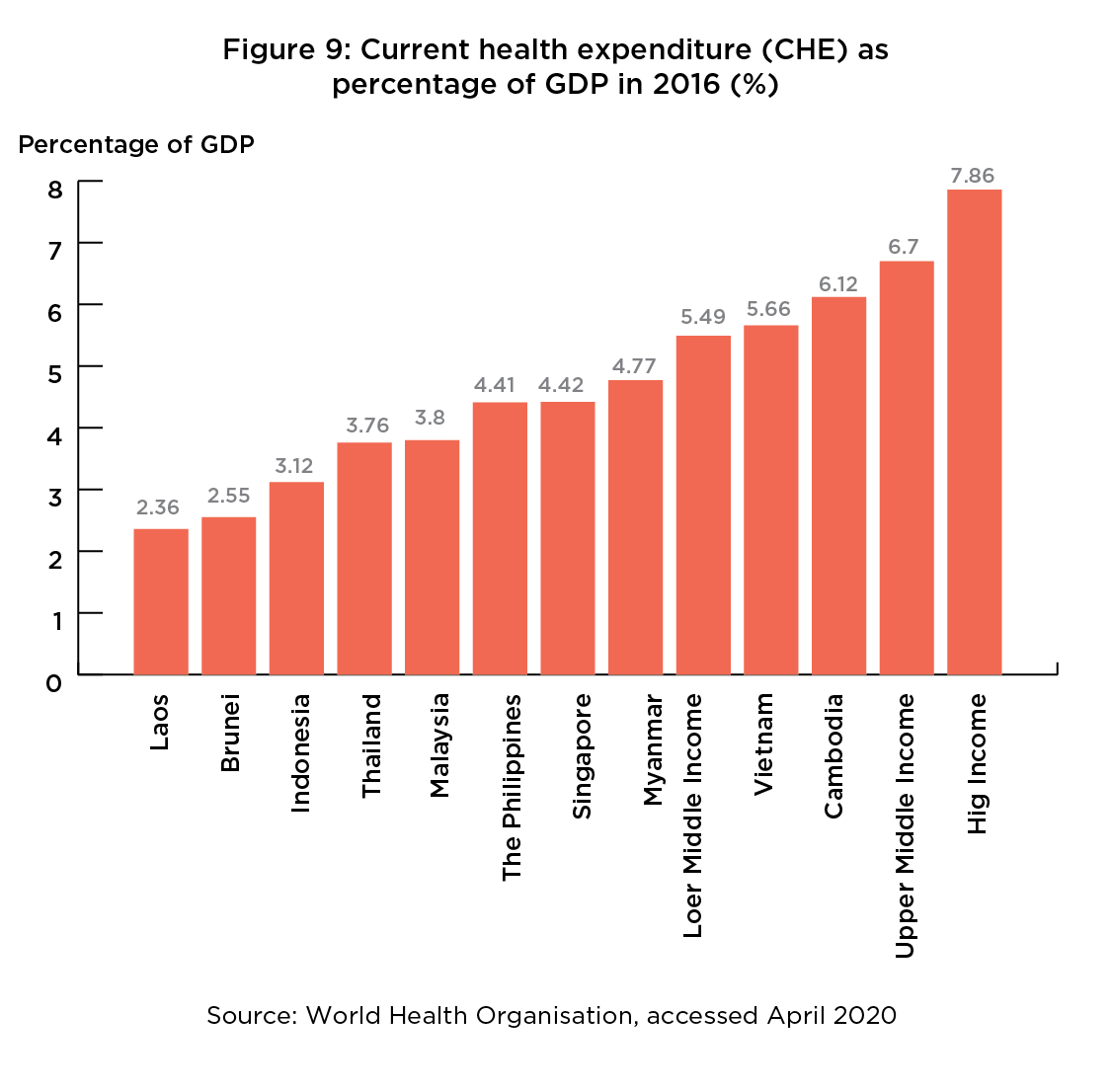

Figures from the World Health Organisation are revealing: the majority of ASEAN Member States with the exception of Vietnam and Cambodia allocated a smaller proportion of their resources towards healthcare compared to the average for lower middle income countries (as defined by the World Bank), and ASEAN collectively allocated lower amounts than upper middle income countries (see Figure 9). This would indicate a lack of focus on public health for many ASEAN countries, which may change post-pandemic.22

- Building a competitive ASEAN single market: for multinationals who seek to diversify their future production bases (instead of producing their goods locally) , many will no doubt turn to Southeast Asia for alternative manufacturing sites. ASEAN must be cognizant of these trends and expedite liberalisation reforms and push ASEAN towards a single market in order to better compete with larger markets such as China and India.

-

*Current health expenditure as a share of GDP provides an indication on the level of resources channelled to health relative to other uses. It shows the importance of the health sector in the whole economy and indicates the societal priority which health is given measured in monetary terms.

**It should be noted that higher health expenditure does not always produce better health outcomes and values. While Cambodia spends a higher proportion of resources towards healthcare than Singapore, the latter scores higher in terms of life expectancy.

-

-

- Guarding against protectionism: the COVID-19 pandemic arrives on the back of ongoing disruptions to global trade caused by the US-China trade war, China’s economic slowdown and internal shift towards domestic consumption, and the UK’s ongoing and uncertain disengagement from the European Union. Depending on the future course of this pandemic (particularly the economic impact), present public skepticism towards globalization may heighten.

As middle-power open economies, ASEAN will have to strive harder to defend the global rules-based trading order from which it benefits from. Regional trade agreements such as the Regional Comprehensive Economic Partnership (RCEP) can serve as multilateral mechanisms to push back against protectionist sentiments, while also bolstering ASEAN centrality and give the region a louder voice in managing great power relations in the region.

- Guarding against protectionism: the COVID-19 pandemic arrives on the back of ongoing disruptions to global trade caused by the US-China trade war, China’s economic slowdown and internal shift towards domestic consumption, and the UK’s ongoing and uncertain disengagement from the European Union. Depending on the future course of this pandemic (particularly the economic impact), present public skepticism towards globalization may heighten.

-

Conclusion

The rapid spread of COVID-19 has led to significant disruptions in global supply chains, with implications for the economic wellbeing of ASEAN. This is due to both the over-dependence of many global supply chains on China (the first epicentre of the outbreak), as well as the inflexible nature of modern supply chains. There are already indications of the economic fallout of the outbreak in China reaching Southeast Asia, with locally-based manufacturers reporting their worse PMI data on record in March 2020, due in part to supply chain disruptions.

There are ultimately several scenarios of how this pandemic and the economic fallout it will bring will play out, from a swift containment of the virus and supply chains eventually recovering within 2020, to uneven recoveries and an onshoring of production amidst rising protectionist sentiments. Multinational manufacturing firms hoping to hedge against future disruption risks can either choose to diversify their manufacturing bases to other countries or produce more goods locally by taking advantage of automation and fourth-industrial revolution technologies. Recent studies suggest the latter process is already underway.

Expected dramatic changes in global trade and supply chains will demand a response from ASEAN in order to maintain international relevancy. The bloc should respond by advocating for greater intra-ASEAN trade and investment to reduce dependency on external markets, as well as pushing towards a single market in order to attract future investors looking for alternative production bases away from China. ASEAN policymakers will also have to be cognizant of the importance of public health as a new dimension of global trade, and guard vigilantly against any rise in global protectionism through multilateral mechanisms such as RCEP.

1World Meters, ‘COVID-19 Coronavirus Pandemic’, accessed on April 3, 2020.

2Bloomberg, ‘Biggest Factory Closing Since World War II Hits U.S., Europe’, March 2020.

3(Webinar) The Economist: Coronavirus outbreak – economic and business implications, February 2020.

4National Bureau of Statistics of China, ‘Purchasing Managers Index for February 2020’, March 2020.

5Ibid.

6IHS Markit, ‘IHS Markit ASEAN Manufacturing PMI: PMI tumbles to record low in March amid global COVID-19 pandemic’, April 2020.

7Ibid.

8Ibid.

9Reuters, ‘In Malaysia’s Silicon Valley, fortunes flip as virus wrecks trade war gains’, March 2020.

10Nikkei Asian Review, ‘Cambodia’s garment industry hangs by a thread’, March 2020.

11 The Star, ‘Covid-19: Indonesia waives income tax for manufacturing workers for six months’, March 2020,

12Control Risks, ‘New global scenarios for COVID-19’, April 2020.

13CIMB ASEAN Research Institute: ‘CARI Viewpoint: ASEAN Roundtable Series on Malaysia-Thailand: Towards Connectivity Beyond Borders’, February 2020.

14Nomura, ‘US-Sino trade friction: not all a lose-lose outcome for Asia’, November 2018.

15Ibid.

16SHEA, ‘COVID-19 and the Workplace Part 1: Global Supply Chain Disruption’, March 2020.

17Kearney, ‘Trade war spurs sharp reversal in 2019 Reshoring Index, foreshadowing COVID-19 test of supply chain resilience’, April 2020.

18Ibid.

*China, Taiwan, Malaysia, India, Vietnam, Thailand, Indonesia, Singapore, Philippines, Bangladesh, Pakistan, Hong Kong, Sri Lanka, and Cambodia.

19Ibid.

20Harvard Business Review, ‘A More Sustainable Supply Chain’, March-April 2020.

21International Finance, ‘Epidemics in China: Reducing global supply chain risks’, March 2020, Harvard Business Review, ‘A More Sustainable Supply Chain’, March-April 2020 issue.

Research Director: Hong Jukhee

Editorial Team: Mohd Imran Said Mohd Shamsunahar, Eleen Ooi Yi Ling, Nor Amirah Mohd Aminuddin